Article Text

Abstract

The 2008 global financial crisis, precipitated by high-risk, under-regulated financial practices, is often seen as a singular event. The crisis, its recessionary consequences, bank bailouts and the adoption of ‘austerity’ measures can be seen as a continuation of a 40-year uncontrolled experiment in neoliberal economics. Although public spending and recapitalisation of failing banks helped prevent a 1930s-style Great Depression, the deep austerity measures that followed have stifled a meaningful recovery for the majority of populations. In the short term, these austerity measures, especially cuts to health and social protection systems, pose major health risks in those countries under its sway. Meanwhile structural changes to the global labour market, increasing under-employment in high-income countries and economic insecurity elsewhere, are likely to widen health inequities in the longer term. We call for four policy reforms to reverse rising inequalities and their harms to public health. First is re-regulating global finance. Second is rejecting austerity as an empirically and ethically unjustified policy, especially given now clear evidence of its deleterious health consequences. Third, there is a need to restore progressive taxation at national and global scales. Fourth is a fundamental shift away from the fossil fuel economy and policies that promote economic growth in ways that imperil environmental sustainability. This involves redistributing work and promoting fairer pay. We do not suggest these reforms will be politically feasible or even achievable in the short term. They nonetheless constitute an evidence-based agenda for strong, public health advocacy and practice.

- SOCIO-ECONOMIC

- SOCIAL INEQUALITIES

- POLICY

- Health inequalities

- INTERNATIONAL HLTH

Statistics from Altmetric.com

Introduction

It has been 8 years since the 2008 financial crisis and the near collapse of the global capitalist economy. The proximate causes of this crisis are well known. A decade of banking deregulation paved the way for a surge in subprime mortgage lending in the USA and risky lending to a real estate boom in the Eurozone. When the real estate bubble deflated, so did the capital of many of the world's banks. The world's richest nations organised unprecedented public bailouts of failing banks, estimated at $11.7 trillion. They employed a suite of monetary policies,1 including direct subsidies and ‘quantitative easing’, where central banks create new money to purchase securities held by private banks (including ‘toxic’ subprime mortgages) to recapitalise these banks. Intended to inject new loans into the ‘real economy’ of production and consumption, much of this new money went instead into the same speculative risk-taking by investment banks that helped precipitate the 2008 global financial crisis.2 This set off another round of asset inflation (primarily in stocks and real estate) which one report estimates boosted the wealth of the UK's richest 5%, those most likely to own such investment assets, by an average of £215 000 per household.3

Meanwhile, the real economy of production and consumption (in which people are employed, earn income and consume products made by other people) crashed. To give this economy a boost, several of the world's richest governments initiated public stimulus spending, estimated globally at $2.4 trillion in the first few years after the 2008 crisis.4 While many countries have now statistically ended their recessions (defined as two consecutive quarters of negative economic growth), their recovery has a long way to go before it is meaningful for the majority of affected populations. The recovery has been described as ‘jobless’,5 with economic growth rates driven more by the rise in the value of financial assets than by increased employment or manufacturing outputs. In the USA, the number of people in non-farm employment only recently began to reach and surpass the 2007 level in 2014, but with population growth the unemployment rate has yet to recover.6 Globally, by late 2013 unemployment numbers were 69 million greater than in 2007, with the rise concentrated among young adults.

Stimulus spending increased governments’ debt-to-gross domestic product (GDP) ratios, especially with many counties’ GDP slowing or even reversing. By 2010, the brief period of government spending to jump-start a global economy in recession gave way to the austerity agenda, the belief that deep budget cuts in public spending were necessary to rekindle economic growth. This belief that now holds most of the world's nations and populations in its unhealthy grip.

The global severity of the 2008 crisis is often regarded as unique. A historical view, however, shows that its proximal causes and policy responses share striking similarities with financial crises of the recent past. As the US Financial Crisis Inquiry Commission report into the causes of the crisis concluded, “The greatest tragedy would be to accept the refrain that no one could have seen this coming and thus nothing could have been done. If we accept this notion, it will happen again.”7 Rather, the 2008 crisis, subsequent recession and government austerity programme are best understood as recent consequences of a nearly 40-year uncontrolled experiment in neoliberal economics.

A brief account of the backstory: neoliberalism and structural adjustment programmes

The basic tenets of neoliberalism, a modern extension of the classical liberalism of such 17th and 18th century theorists as Jeremy Bentham, John Stuart Mill and Adam Smith, are generally credited to Friedrich von Hayek. Writing in the 1940s, Hayek argued that governments should not interfere with markets.8 The economy is simply too complex to manage, and so according to Hayek, it is best to let markets regulate themselves through free trade, strong property rights and minimal government interference, balanced by the ‘rational’ choice of a world of sovereign individual producers and consumers. Critics of neoliberalism have characterised it as the belief that “the nastiest of men for the nastiest of motives will somehow work for the benefit of all.”9 In high-income (Organisation for Economic Co-operation and Development) countries, Keynesian economics, with its call for greater government involvement in the economy, trumped neoliberalism during the post-WWII ‘thirty golden years’ of economic growth,10 heralding progressive taxation, new social protection programmes and sharp declines in income inequalities.11

In the 1970s, however, high inflation and low economic growth (‘stagflation’) created a political space for neoliberal economics to enter. It did so, first in Chile in 1973 with the US-supported coup against the socialist government of Salvador Allende. It then began globalising with the election in the 1980s of conservative governments in the USA (Reagan), UK (Thatcher), Germany (Kohl) and other economically advanced countries.

The 1970s developing world debt crisis lent further support to the expansion of neoliberal economic policies. To prevent sovereign defaults (where governments became unable to pay international creditors), the International Monetary Fund and World Bank gave loans and grants to the most heavily indebted countries, but with radical free-market economic conditionalities (the term used to describe conditions attached to loans, debt relief or development assistance): extensive privatisation of state assets, tax reforms to attract foreign investment, public debt and deficit reduction and rapid trade liberalisation. The assumption was that these policies would allow governments to continue debt payments to foreign creditors while stimulating economic growth. The reality is that, although succeeding in embedding neoliberal economics in many developing nations, these policies failed to improve economic growth in the two regions of the world most encumbered by structural adjustment, Latin America and Africa.12

Central to structural adjustment was a reduction in social protection spending by governments, which subsequent analyses found to be a main cause of increases in poverty and inequality in affected countries.13 The consequences for health were predictable. By increasing (or failing to reduce) poverty and inequality, two major risk conditions for preventable disease, structural adjustment slowed-down or reversed earlier health gains, affecting vulnerable populations such as the poor, rural populations, women and children.14–17

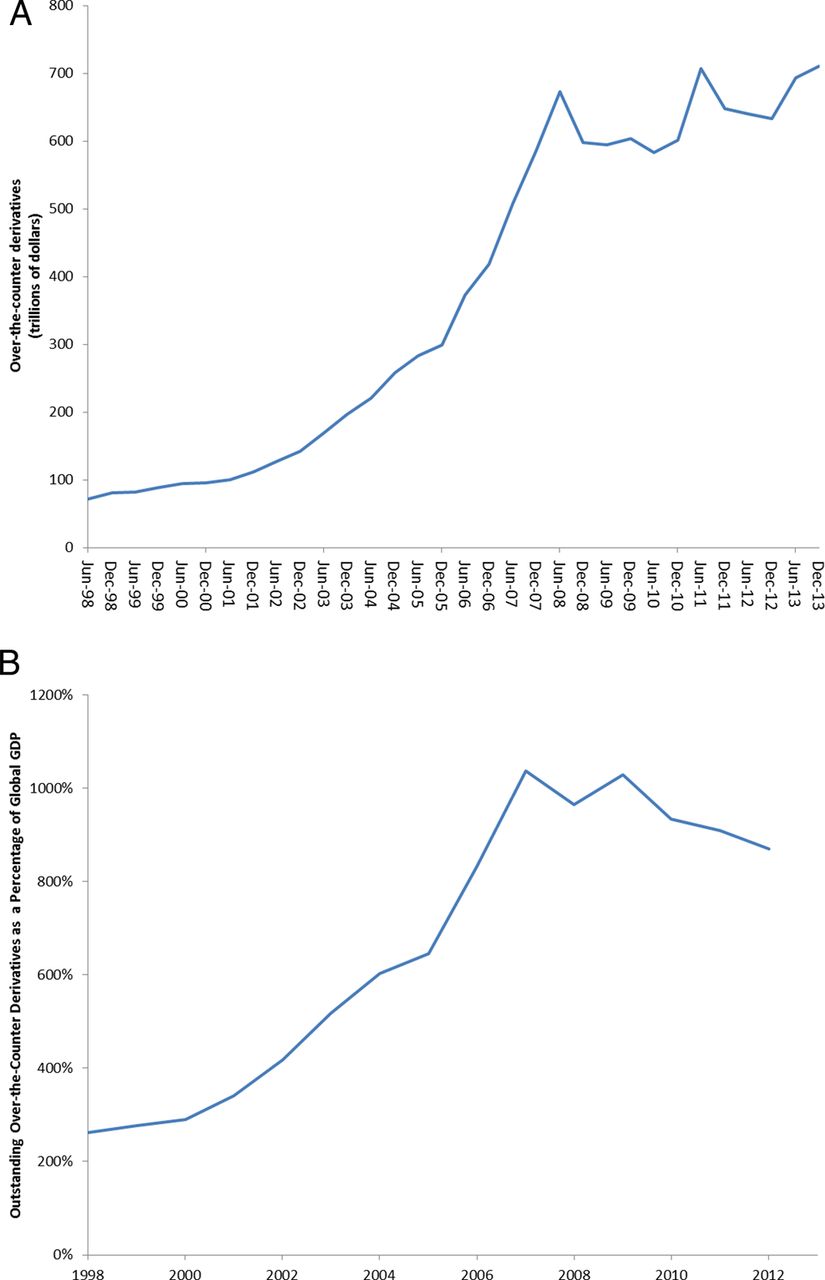

The ‘roll-back’ of structural adjustment (reductions in government health and social protection spending) was accompanied by a ‘roll-out’ of neoliberalism in the form of liberalised financial markets. Aided by the removal of capital controls (restrictions on money flowing in or out of a country), deregulated banking rules and new digital technologies, investors found that it was easier and faster to make money from money than from lending to the real economy. The resulting surge in economic financialisation is unprecedented. In the year 1980 the total value of all financial assets in the world was roughly equal to that of the world's gross economic product.18 By 2012 the value of outstanding derivatives (investment contracts which value is ‘derived’ from underlying financial assets such as commodities, stocks, currencies, market indexes and interest rates) exceeded $710 trillion, or almost 10 times the total value of the world's gross economic product (figure 1A, B).19 The huge growth in this highly leveraged and unregulated financial market was one of the drivers of systemic global financial risk that preceded the 2008 crisis. Although declining slightly in the immediate aftermath of the crisis, the value of these derivative then soared by over $100 trillion, one suggested reason for the high profits reported by recapitalised banks during this period.

Rise of over-the-counter derivatives (above) and as percentage of global economic product (below) (1998–2013).70

Enter austerity

Since 2008 the International Monetary Fund, European Central Bank and European Commission have promoted austerity as a remedy to rising public debt and slow recoveries. Austerity measures are almost identical to the discredited structural adjustment conditionalities of the 1970s.20 Unlike structural adjustment, austerity this time is global, affecting countries across the low-income to high-income scale—including those, such as Germany, Australia and Canada, where public deficits are well within the bounds of prudent fiscal management. This fiscal contraction is most severe in the developing world, with austerity “affecting 5.8 billion people or 80 percent of the global population in 2013 [and is] expected to increase to 6.3 billion or 90 percent of persons worldwide by 2015.”4 Nearly one-quarter of developing countries are undergoing excessive contraction, defined as cutting public expenditures (as a percentage of GDP) below prefinancial crisis levels.21

Despite the IMF's recent stated retreat from ‘excessive’ austerity, and although showing more flexibility with the present financial crisis than with earlier structural adjustment, it is arguably the case that “there has been no meaningful rethinking in the application of dominant neoliberal macro-economic policies… In other words, the IMF is using the financial crisis to promote a further cutting back of the state in the midst of the ongoing social outfall of the financial crisis.”22 A cross-national study of policy choices in Europe during the crisis found that countries receiving IMF loans were significantly more likely to pursue austerity policies and, when they did, were four times more likely to reduce healthcare budgets than were non-IMF borrowers, even after correcting for the severity of those nations’ economic recessions and debt levels.23 Not all governments have pursued these policies, but many have implemented some if not all of the neoliberal platform.

Neoliberalism's health impacts: from crisis to recession to austerity

Short-term health effects

Proximally, the financial crisis and its aftermath is having mixed health impacts. Declines in disposable income show some reduction in discretionary expenditures on tobacco or excess alcohol consumption, although binge drinking has been rising in some countries. Poverty rates, homelessness, consumption of low-cost obesogenic food, unemployment-poverty/insecurity-related stress levels are all expected to increase, and have done so in some of the worst affected countries.24 ,25 Taking a few examples, EuroStat data, one of the only available sources of comparative information across Europe, reveals a marked rise in food insecurity since 2010, when austerity began. The rise corresponds to 13.5 million additional Europeans who are unable to afford a healthy diet.26 Suicide rates since the crisis indeed have increased by 12 to 15% in the worst affected European countries.27 ,28 An early study of the health impacts of this policy choice in Europe is revealing.29 Healthcare budgets were cut by 20% or more in several countries; in Greece, the hospital budget cut was more than 40% even as postausterity demand for hospital care rose by 25%.25 One dramatic outcome of the Greek cut has been the rise in HIV cases following elimination of prevention and needle-exchange programmes (figure 2). Across Europe there has been a reversal in downward trends in ‘unmet need’—people who report being unable to access medically necessary care. This is sharpest in countries with commodified health systems and in the grip of austerity, totalling over 1.5 million additional people unable to access healthcare.24

Long-term health effects

The long-term health effects of the financial crisis, Great Recession and austerity largely depend on how they affect people's employment and working environments. Not all employment is healthy.30–32 Longer term unemployment, combined with shrinking protection supports, however, is likely to lead to unhealthy coping behaviours and chronic poverty. The quality of employment is also deteriorating in a deepening of labour market restructuring that began in the early 1980s, leading to increased economic insecurity even for those holding jobs (figure 3).33

Increasing economic insecurity of workers as measured by time-related underemployment (employees who wish to work more hours, are available to work more, and are below full-time working hours).73

Labour market restructuring in this era has been accompanied by a continuing decline in unionisation rates in advanced economies, and particularly since the 1980s (figure 4). UNCTAD globally estimates that the share of global economic production going to labour versus capital fell from just over 65% to under 54% between 1980 and 2011.34 These trends have led to a new term, the ‘precariat’, characterised by people working in short-term jobs, without recourse to stable occupational identities or careers, reliable social protection support and protective regulations (figure 5).35 Precarious work is common in most countries. About four of five American workers in insecure or part-time minimum wage jobs are projected to experience working poverty at some point in their lives.36 Germany, considered by some the economically healthiest country of the Eurozone, has the second highest percentage of low-earning and part-time workers (so-called ‘mini-jobs’).37 The UK is facing criticism for the rise in its ‘zero hours’ contract employment (where the employer is not obliged to provide a minimum number of hours),38 and for a recovery mainly found in jobs that are part-time or temporary. The UK median wage continues to fall as most of the income growth accrues to the top 1%.39 It is not alone in this trend, with informal labour markets predominating in many Latin American cities (despite some gains in poverty reduction) and characterising over 95% of the workforce in India.40 Africa, the latest region to post impressive postfinancial crisis growth gains, has failed to see this benefit African youth, the majority of whom are unemployed or grossly under-employed.41 China is experiencing increased labour unrest with the global economic slowdown. Some employers have been unable, or simply unwilling, to meet their payroll costs or have threatened to move to lower wage neighbouring countries if workers demand a fairer share of the manufacturing wealth they have helped to create.42

Declining rates of union membership.74

Declining wage shares in the economy.75

What must be done?

Without radical reforms, neoliberal policies will continue to imperil the world's population. Below we summarise four leading policy reform areas that can move us towards a healthier body economic.

Re-regulate finance

Restore the rules that separate commercial from investment banking and restrict investment bankers from engaging in speculative investing on their own behalf (‘proprietary trading’).43 By 2015 US banks will have to comply with a new postfinancial crisis rule separating these two forms of banking, although they are aggressively pursuing ways around the new rule.44 UK banking reforms are even milder than those in the USA, ring-fencing only one-third of commercial from investment banking. This watering down of re-regulation has been attributed to heavy lobbying by the financial sector.45 Internationally, efforts to reduce the risks of speculative investing arising from under-capitalised banks are insufficient, requiring banks on global average to retain just 3% in what they hold in deposits relative to what they loan or invest.46–48 It was the widening asset to equity ratio, with banks leveraging greater proportions of their assets, which led, in part, to the 2008 financial crisis.

There is also a need to stem the huge growth in derivatives. This may begin to happen if a 2009 G20 commitment to create a public exchange system for derivatives is implemented, allowing for greater transparency and potential regulation of internationally risky speculation.49

A fuller re-regulation of global capital, however, remains elusive. This is in part because it demands a global social response that several countries beholden to the increasing economic and political power of their financial elites appear unwilling to embrace. Meanwhile, the incomes of the world's leading hedge fund managers rose by 50% in 2013, with one manager taking home $5.7 billion in the past 2 years alone.50

Reject austerity

Neoliberal economic policies have gone largely unchallenged despite their clear failings. Explanations for this situation include a lack of alternatives that will be accepted by economic elites, ideological commitments to neoliberal principles like a ‘minimal state’ and erroneous economic models. In one instance a highly cited analysis concluded that when government debt exceeded 90% of GDP economic growth faltered; therefore austerity was the better policy.51 A graduate student later identified a spreadsheet error in the study that, when corrected, showed no negative association of public debt with negative growth.52 In a second instance, the IMF incorrectly estimated a quantity known as the ‘fiscal multiplier,’ which measures the impact of public spending on the overall economy. Initially IMF economists assumed an average fiscal multiplier of 0.5: For every dollar of new government spending during its crisis, the economy would lose 50 cents (0.5 of a dollar). In 2013 a recalculation performed by the IMF found that the fiscal multiplier for public spending actually ranged between 0.9 and 1.7, and was most likely at the higher end of the estimate.53 ,54 For every dollar in new government spending, up to $1.70 in economic growth would occur. In the postfinancial crisis environment, government spending is thought to have on average a 1.6 fiscal multiplier effect.55

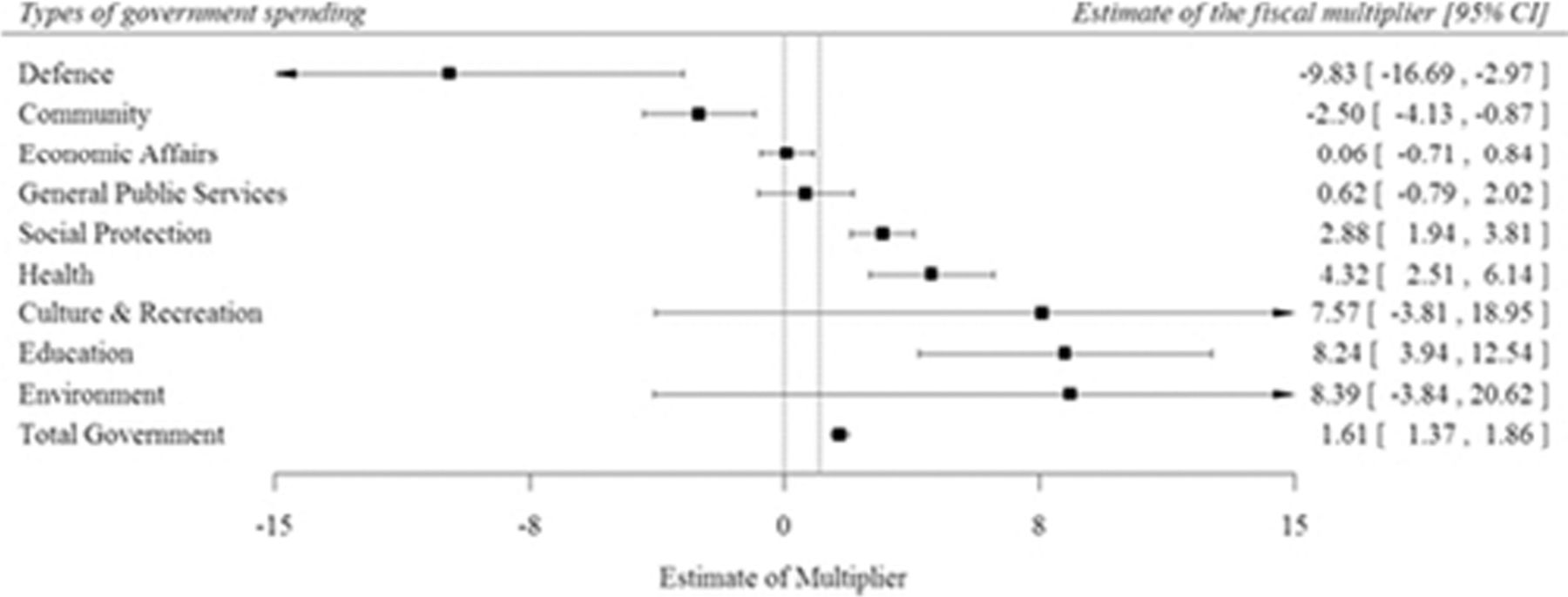

Sector-by-sector analyses have shown much greater fiscal multiplier impacts in health, education and environmental protection, and an economic drain for public spending in defense (figure 6).56 Canada's finance department, using ‘prudent estimates’, forecast in 2010 that every dollar in public spending for new infrastructure, housing or measures for low-income households and the unemployed would boost the economy by between 1.3 and 1.5. Individual tax cuts, however, would cost the economy (0.9), with business tax cuts the worst of all (0.2).

Fiscal multipliers (1995–2007).56

Simply put: the economic logic for austerity has been shattered. Government spending in health and social protection not only improves health equity and contributes to social stability but also boosts economic growth. Countries that increase social spending during economic recessions recover much faster (figure 7). As the world is beginning to learn, austerity in times of economic recession and gross income inequities makes things worse for the poor, but better for the rich.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Government spending increases economic recovery.30

Increasing progressive taxation

To reverse this inequitable spiral, governments must tax progressively. In many of the world's high-income countries, progressive taxation rates (on corporate profits, high incomes and capital gains) have fallen steadily, particularly in the Anglo-American countries. Most of the world's economies, even by conventional GDP growth measures, can withstand large increases in present taxation rates. A rise in the US marginal income tax rate from its present historic low of 35% to its previous high of 68% would have no statistically significant negative impact on the economy. It would, however, substantially reduce poverty and inequality; and through increased public spending, likely reduce unemployment.57 The IMF, more conservative in its estimates, nonetheless reaches a similar conclusion for marginal rates of 60%, which it argues would actually boost economic growth.58

If progressive taxation rates had remained at levels common in the 1980s, there would be no fiscal crisis or need for austerity. As one more recent example, using monetized (constant dollars) value of the Global Economic Product and the amount captured by the effective global tax rate, the amount of private capital falling outside the bounds of taxation jumped from $28 trillion in 2004 to $58trillion in 2012, more than doubling in just 8 years.59

There is no shortage of wealth, but a hazardous misallocation of it. The implications for health are straightforward, especially in low-income and middle-income countries. A recent study of taxation policies and universal health coverage in low-income and middle-income countries found that taxation was a critical determinant of health system strength.60 Health spending rose in tandem with (largely) progressive tax revenues from income, capital gains and profits; but fell when tax revenues relied on (largely) regressive consumption taxes (on goods and services). Higher rates of postneonatal, infant and under-5 mortality were also associated with regressive tax increases, likely because such increases priced essential goods beyond the means of poorer families.

Tax financial transactions

Although tax progressivity is the responsibility of nations, a globalised financial system requires global systems of taxation. The 2008 financial crisis has reinvigorated debate over the need for a financial transaction tax (FTT), not simply to dampen harmful speculative investing (its original intent) but to help support transfers for global health and social development and finance global public goods, such as climate change prevention/mitigation. The revenues of such a tax if implemented globally at the low rate of 0.05% range between $410 billion (if applied only to bond and share sales) to $8.63 trillion (if also applied to derivatives and over-the-counter trades).61 In January 2013, 11 European Union countries agreed to implement a FTT at a low level rate that would raise about €35 billion annually.62 Some 63 countries have stated their support for an FTT, if revenues from such a tax were (at least partly) used to finance global development initiatives. However, other countries are strongly opposed to a FTT, including the USA, the UK (both with powerful international banking sectors), China and India.

There is also a need to clamp down on tax evasion through the use of offshore financial centres, commonly referred to as ‘tax havens.’ International banks in these offshore centres shelter as much as $32 trillion in personal wealth. Estimates of foregone annual tax revenues on growth on this principal alone range between $180 and $250 billion annually.63 ,64 Since the 2008 financial crisis there has been an almost threefold increase in ‘wealth management’ funds held in tax havens by the top 10 investment banks.65 There is momentum for reform, however, with the G20 in 2013 committing to a system of finance reporting such that taxes are paid in the jurisdictions where profits or incomes are created,66 which the G20 agreed to implement by 2018.67

Conclusion

Forty years of a dominant discourse of individualism has bred a cynicism towards organised politics that only strengthens the neoliberal agenda. Even as political participation is thriving in many low-income and middle-income countries (at least where it is not violently suppressed), it is waning in most of the democratic high-income countries. Robert Reich, writing about politics in the USA, argues that this is the intent of power elites: “to make us all so cynical about government that we give up…making it easier for the moneyed interests to get whatever they want,”68 a caution now borne out empirically.69

Yet there is no reason why governments could not re-regulate global finance, strengthen rather than weaken labour markets and tax progressively both within their borders and globally. The ‘1%’ can be tamed. However, despite the growing chorus of antiausterity critics across political spectra, multilateral institutions and evidence-based academic disciplines—to the point that some are declaring austerity ‘dead’—many politicians do not seem to be getting the message. We need to work harder to reclaim the narrative: we do not have a fiscal crisis. We have a crisis of inadequate taxation. We are not living in conditions of economic scarcity. We are living in conditions of extreme inequality. Our voices of opposition to neoliberal globalisation need to be raised louder and stronger. Evidence and ethics are on our side.

References

Footnotes

Contributors RL and DS jointly developed the article. RL wrote first drafts which DS revised. Both authors have read and approved the final copy.

Competing interests None declared.

Provenance and peer review Commissioned; internally peer reviewed.