Article Text

Abstract

Background Tobacco displays at the point of sale (PoS) are an important means for the tobacco industry to communicate with consumers. With regulations prohibiting PoS displays recently having come into force in Ireland, passed into law in England, Wales and Northern Ireland and some Australian states, and being considered in New Zealand, Finland and Brazil, this is an increasingly important issue. This study explores the nature of displays, the extent to which they are tobacco industry funded, and the relation between the tobacco companies and retailers.

Methods Three areas were chosen to gain a snapshot of PoS displays in England. Over 100 retailers were visited, with interviews taking place on site. Information was gathered on the type and size of tobacco display, who was paying for the display, requirements and incentives, and visits by industry representatives.

Results The majority of retailers had gantries provided by tobacco companies. A minority of these were fitted with automated dispensers called retail vending machines. Attractive lighting and colour were often used to highlight particular products. Most retailers were being visited by industry representatives who checked displays. Some retailers also reported incentives offered to them for displaying products.

Conclusions The results suggest that the tobacco industry presence and control in the retail environment is significant. Tobacco companies overwhelmingly provided tobacco gantries in the shops surveyed and influenced displays through a combination of requirements and incentives. The extensive involvement of tobacco companies in providing and monitoring retail displays suggests the importance of implementing policies to end this form of advertising.

- Tobacco

- smoking

- point of sale

- marketing

- retail

- advertising and promotion

- tobacco products

Statistics from Altmetric.com

Background

Tobacco point-of-sale (PoS) marketing has become an increasingly important area for the tobacco industry. As restrictions on the ways that manufacturers can promote their product increase, the packaging and display of tobacco products have become the primary means by which the industry promotes its products and are, therefore, a central issue for tobacco control. PoS displays have been shown to promote uptake of smoking by young people, increase tobacco consumption and undermine quit attempts in smokers.1 2 A large number of countries have implemented full or partial prohibition of tobacco advertising. Now regulation of PoS tobacco displays is under consideration in a number of countries: there is already prohibition of PoS display and advertising in most Canadian provinces, Thailand and Iceland.3 Legislation came into force this year in Ireland and will come in to force in Norway and most Australian statesi from 2010. Legislation has been passed into effect that will permit similar regulations in England, Wales and Northern Ireland (Health Act, 2009) and is under consideration in Scotland; and PoS regulation is also being considered in New Zealand, Finland and Brazil. Further, the inclusion of PoS regulations may be an important issue to consider for countries that are yet to implement an advertising ban under the WHO Framework Convention on Tobacco Control (FCTC) agreement.

It has been shown that smoking prevalence increases as the amount of advertising increases.4 An argument often used by those opposing regulation of PoS tobacco displays is that these displays are only intended to make people who smoke aware of new brands. In fact, the evidence suggests that PoS displays act as a form of advertising and they have been defined as such under guidelines to Article 13 of the FCTC.1 5 6 As a report for Cancer Research UK emphasised:‘PoS display is then a fundamental part of marketing. It tells both potential and existing customers of the products that are available to them; the key attractions of each product, and; provides them with reasons for both trial and adoption. It also enables the tobacco industry to… maximise the effectiveness of their other marketing tools—most notably packaging, branding and distribution.’1

The prominence of cigarettes in shops and their ready availability give the impression that tobacco use is normal and socially acceptable. Further, there is evidence that PoS displays affect smoking initiation by children,3 7–9 and may affect the smoking behaviour of established smokers.3 6 10

The importance of PoS marketing to tobacco companies has increased as greater restrictions on other forms of advertising have been introduced. As observed in the Australian context:‘When above-the-line was banned, the retail environment became the front line for brand building, absorbing massive resources and being seen as the primary site for sustaining relationships with the consumer. When retail was restricted by some states, the industry conceded only incrementally and under duress.’11

Increased spending on the retail environment has been noted in several countries, including Canada, the USA, Australia and New Zealand.ii,5 By 2007 US tobacco companies were spending 85% of their promotional budget in the retail environment.3 In Australia retailers receive more money for displaying tobacco than they do for other types of product.12 North American studies have also found significantly more PoS tobacco promotions near schools and in low-income and minority neighbourhoods than in better educated, higher-income, predominantly white neighbourhoods.13 14

The kind of promotion focused around PoS and utilising retailer strategies to sell a product is referred to as ‘push promotion’. Lavack and Toth used historical evidence from tobacco industry documents to show how tobacco companies have increasingly focused attention on the retail environment and push promotion as a response to restrictions on advertising. They suggest that efforts have focused on dominant positioning of the company's products at PoS to suggest popularity, the work of sales representatives in achieving space for and visibility of products at PoS through contracts with retailers and the provision of display cabinets.15 Recently, data have been gathered on tobacco company incentive programmes. In the USA, Feighery et al found promotional allowances and special offers in return for control over the retail environment.16 John et al found that contracts among retailers were widespread, companies controlled advertising in stores and the role of the store owner was passive.13 Moreover, they reported that some retailers resented this amount of control and the coercive nature of contracts. They also found incentive programmes in the form of ‘buybacks’ (temporary price reductions).

Turning to the context in England, in 2003 the Tobacco Advertising and Promotion Act (TAPA) prohibited tobacco print media and outdoor advertising, some promotional activities and tobacco sponsorship of domestic sporting events. Restrictions on PoS advertising followed in 2004, which allowed only one A5 sized (15×21 cm) poster advertising tobacco in store with 30% of that area taken up with a health warning. A study of the display of tobacco products in retail premises in England was conducted for Action on Smoking and Health (ASH) in 2008.17 It found that tobacco displays were a prominent element at the point of sale; and that novel devices, colour, lighting and blocks of product were used to highlight tobacco products and gain prominence for a brand. However, it was not possible to gather much data on incentives for retailers.17 This study aims to build on the previous evidence from England by gathering data on the nature of displays, the extent to which they are tobacco industry funded and the relationship between tobacco industry and retailers. We hope to provide a picture of the English context where, unlike the context for the US studies described,13 16 PoS advertising is tightly restricted at a time immediately before further restrictions are adopted.

Methods

The study was designed to provide a snapshot of tobacco product PoS displays and relationships between retailers and tobacco companies before legislation banning such displays in England (Health Act 2009). Four areas were sampled: two in London (Shoreditch and Soho) and two in Nottingham (Aspley and Radford). The areas were selected for convenience, but also to gain some variation in terms of population and area. Aspley was the most deprived area with an index of multiple derivation (IMD) score of 62, followed by Shoreditch (49/50), Radford (38) and then Soho (26). The adult smoking prevalence in each area also varied with Aspley at 48%, Shoreditch 38–41%, Radford 34% and Soho 33%.18

A brief survey was designed to gain data on the type and size of tobacco display, who was paying for the display, requirements and incentives, and visits by industry representatives. In the two London areas tobacco retailers located within a half mile radius were identified. The centre for the radius was selected to be roughly central to the two areas of interest (Shoreditch and Soho). For the Nottingham sample this area was extended owing to a lower density of shops. Shops were identified online in the first instance, using the websites http://www.Yell.com and http://www.192.com, and then additional shops were added as they were discovered while the survey was being conducted.

Researchers completed a form based on observation of the appearance of the displays. This included the type of outlet (‘multiple’, ‘independent’ or ‘forecourt/garage’); how are the cigarettes and other tobacco products displayed? (Purpose-built cabinet, standard store shelving or counter, vending machine or other (describe)); how large is the display? (standard (1 metre), 1.5 times standard, twice standard, etc) and is there anything about the display that makes the tobacco particularly stand out? The person behind the counter was then approached and asked if they had time to undertake a short interview.

Interviews were designed to be brief so as not to take people away from their duties for too long. Interviews took place on site with the person behind the counter, unless there was someone more knowledgeable also working. The survey was designed to occur over a short space of time; therefore the decision was made to talk with whoever was on site, rather than to pay repeat visits in order to interview the manager or owner. It was decided as the study progressed to exclude companies with multiple outlets (multiples) from the interview as it was found that generally tobacco stocking and display matters were handled by the company head office and staff were not able to answer questions. Moreover, we thought it was appropriate not to pursue this as our primary focus was on small retailers who have been the focus of political debate on the impact of PoS regulations.19 20

Interviewees were asked brief exploratory questions in the first instance: who pays for the gantry? Are you offered any further payment or incentives for hosting the tobacco display unit? Do [insert company name] require you to do anything in return for the gantry? How often do [insert company name] representatives (reps) visit? Do any other tobacco companies, who don't pay for the gantry, offer any incentives?

Depending on the answers, these were followed up with prompts such as: if they said they were offered incentives—can you give me some examples? If they said there were conditions attached to the gantry—what sort of things? How do you feel about this? If industry reps visited the store—what happens on a typical visit?

In addition to the survey of retailers, the retail press was investigated to elicit further information on how tobacco products are promoted to retailers and incentive schemes. The publications Convenience Store, Retail Newsagent and The Grocer were monitored for 6 months between March and August 2009 and tobacco promotions were noted.

Results

In total, 113 shops were visited. London shops made up 69% (78) of the sample (40 in Shoreditch, 38 in Soho), and 31% (35) were in Nottingham (24 in Aspley and 18 in Radford). Of the 113 shops, 84% were independent retailers and the remainder were multiples.

Type and size of display

In all of the independent retailers tobacco products were displayed behind the counter. This was true for most of the multiples, except when there was a separate tobacco kiosk. The most common display was the standard contained shelf cabinet or ‘gantry’. Eighty-seven per cent of all shops had these displays. Only nine (8%) shops in the sample stocked tobacco products on standard store shelving and none of these were found to be industry funded. The remaining six shops (5%—all of which were in London) were fitted with automated dispensers that the tobacco industry describes as retail vending machines (RVMs). It is important to note that the sample packs displayed in RVMs are not for sale but are there for display purposes only. The RVMs are operated by the use of an electronic key pad controlled by the retailer (see figure 1).

Example of the type of retail vending machine found in London.

Two-thirds of the displays were a standard size of approximately 1 metre in width, while 12% were one and a half times the standard size and 10% were double or larger. Only 12% were smaller than standard. Seventy-eight per cent of multiple-type shops had displays that were larger than standard, of which two were very large displays (at least 3 metres across) on separate tobacco counters.

The great majority of the gantries found in the sample were eye-catching in some way. Many had lit or colourful top panels, lighting of the products and/or colourful illuminated strips down the sides, while others had clocks or stickers advertising other branded tobacco-related products such as Rizla (a brand of hand-rolling papers). Two particular models of gantry were found to be most common in the independent retailers (64% of stores had one of these two display types—see figure 2); the most common (42%) had a yellow, illuminated top panel and often an illuminated display and blue, lit side strips (see gantry on the left of figure 2).

Example of the two most common types of gantry.

The majority of the displays featured blocks of products, which served to highlight specific brands—this was particularly noticeable with the larger displays, which often used coloured strips to highlight certain brands. Some of the stores also had extra displays for Benson and Hedges rolling tobacco, which had recently been launched, with large price marking attached to the side of displays.

Elsewhere, examples were found of a ‘hanging’ display in three stores (see figure 3). This was in addition to a standard gantry and was prominently displaying BAT products suspended from the ceiling above the till. Two of these stores reported being paid by BAT to have these hanging displays installed.

Example of hanging display.

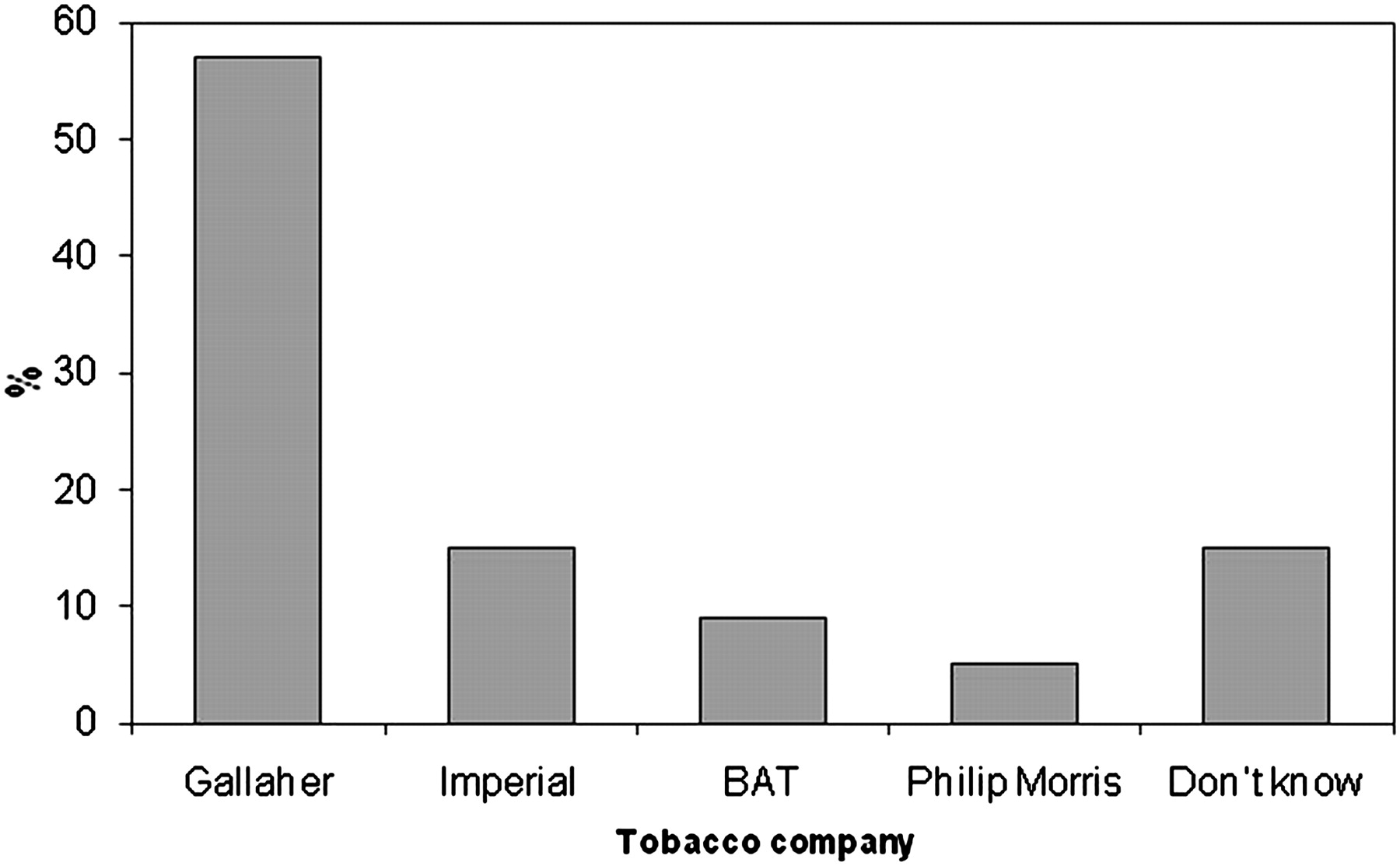

Percentage of displays provided by tobacco company.

Display funding

Of the 95 independent retailers, 76% agreed to talk to us; the remainder were either unwilling or unable to answer the survey questions (they were too busy or did not know about the gantry). Of the 72 retailers interviewed whose store had a gantry or RVM, the great majority (93%) said it had been provided by a tobacco company. Gallaheriii was the most common provider of gantries (57%) followed by Imperial Tobacco (15%) (figure 4). Interestingly, all of the RVMs we collected data on had been provided by British American Tobacco (BAT) and all appeared to be the same type. One of these retailers informed us that he had had a gantry from a different company, until BAT offered him the new RVM display.

Nearly four out of five (79%) retailers who had a tobacco industry-funded gantry had to comply with certain conditions. In all cases where retailers discussed conditions, they reported a requirement to stock the provider company's products in a certain way—for example, on the top shelves, having a certain number of shelves of their products, on shelves at eye level or according to a display plan. A few said that the company reps arranged the gantry for them.

Incentives and relationship with company representatives

Fifty-eight per cent of the shops were visited regularly (once a month or more) by tobacco industry reps, 33% received less frequent visits and only two shops (3%) were not visited by the reps (with the remaining 6% of respondents saying they didn't know or not answering the question). None of the shops where the gantry was not funded by a tobacco company had frequent visits. Most of the visits were to check the display and inform the retailers of new products or promotions. A few retailers reported that the reps would clean the display as well as arranging it or reorganising it with new products or products with promotional offers most prominently displayed.

A minority (about a third) of independent retailers reported getting some kind of incentive from tobacco company reps for selling their products. Most often these were small gifts such as pens, free packs of cigarettes and offers on products. A respondent with a small display box containing rolling tobacco attached to the top of his display said that if he kept it there he would receive free packs next time. Some retailers, however, reported larger incentives. One described a raffle system where shops were entered into a draw and then randomly picked, with the first prize being a total shop refit and the next 200 shops picked receiving £200 of vouchers. Another scheme involved the recording of barcodes from products sold, which could then be redeemed against vouchers for Argos—a large discount store (the respondent had saved up for a digital camera). Another said the shop received points if they maintained the gantry as the rep had arranged it and they could save these up for Argos vouchers. Others mentioned getting vouchers or being paid extra to display a company's product.

The investigation of the retail press found examples of promotions of limited edition products through competitions. To promote Silk Cut limited edition pack designs, a 32-inch LCD television was on offer for texting ‘PREMIUM CUT’ to the given number, while Camel's ‘discover the hidden camel and win £1000’ promotion encouraged retailers to search their copy of Retail Newsagent to find the Camel logo.21 22

Comments from a few retailers showed little enthusiasm for either the displays or the tactics of the tobacco industry reps, with one retailer describing the latter as ‘bullish’ and intimidating. There was concern that the size of displays and the insistence of the tobacco industry reps resulted in retailers stocking far more product than they would if given more choice. One retailer said he would not have such a large display if it were not funded by the tobacco industry. He suggested that the rep's insistence on the display being kept fully stocked with his company's product meant that he had ‘£3000 of dead cash’ and went on to say of the situation: ‘You just want to shift the stock so if a kid comes in late at night you're tempted to sell to them.’

Limitations

This study has a number of limitations: sampling was by location and so not necessarily representative of small retailers across England, interviews were brief, and the person being interviewed did not always know all the details about the gantry and contract. However, the study set out to provide a snapshot of current practices, rather than a comprehensive survey or in-depth qualitative study of retail practices in England. It sought to balance a reasonably large number of shops with providing some qualitative data on limited resources. In this respect it provides a useful picture of the state of tobacco displays as new legislation is considered and gives an impression of the relationship between retailers and tobacco companies, confirming some of what has been found in other countries and adding to the data on England.

Discussion

Our results underline the prominent and eye-catching nature of tobacco displays, even with restrictions on advertising at PoS. They also highlight the control that the tobacco industry has over displays: providing them, requiring their products to be displayed in particular places and even arranging and maintaining displays. It was also found that gantries are fairly standard across shops. Interestingly, in an article in Retail Newsagent at the time of the restrictions on advertising at the PoS in 2004, a spokesman from Imperial Tobacco commented: ‘The fact that we can't advertise means that products have to speak for themselves. Retailers need well-lit, clean stands stocked with an appropriate range to meet all needs.’23

It is illuminating to note that in Ireland, between the first announcement of the proposal to prohibit PoS displays and implementation of the legislation, RVMs became far more widespread; moreover, the RVMs in Ireland are funded by the tobacco industry.24 They are reported to cost in the region of €10 000 (personal communication 2009, Eamonn Rossi, Office of Tobacco Control, Ireland). Investing in these machines provides manufacturers with greater control over displays that can easily be made compliant with the legislation—sample products need only be removed from behind the front glass panel. RVMs also maintain a link to the branding through the use of the electronic key pad which displays all the brands in picture form. Our data point to a similar strategy being used in England by at least one manufacturer. In Ireland RVMs have gone through three stages. In the first stage they were used to display sample products, creating the illusion of a conventional display. From February 2009, in the last few months that point of sale displays were still permitted, manufacturers visited retailers replacing the old display and giving them even greater visual impact by affixing brightly coloured, advertising panels bearing large font price promotions (see figure 5) before being removed to comply with the legislation.24 This ‘sunset’ period before a marketing ban has been observed previously in a Canadian study, including a similar pattern of accelerated promotion in advance of a display prohibition.14 Evidently the installation of RVMs is not necessarily inhibited by proposals to restrict PoS.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

‘Sunset’ tobacco display in Ireland one week before prohibition.

The provision of displays by the tobacco industry, standard nature of displays and the evidence from Ireland are particularly relevant points in terms of a potential prohibition of PoS display. One of the main arguments against a display ban is the cost to the retailer. However, our results suggest that it is likely the tobacco industry would continue to meet these costs, and that standardising cabinets would not be difficult.

It is unsurprising that Gallaher (JTI) and Imperial Tobacco fund the majority of displays in this sample (72%) as between them they control approximately 80% of the UK tobacco market, while BAT only has 5% of the UK market (and 5% of displays in our sample). It is worth noting that the high-cost displays, including hanging displays and all the RVMs, were funded by BAT and make up two-thirds of those displays that retailers told us were funded by BAT. It seems that many of the push promotion tactics described by Lavack and Toth are still being used.15 There is also some evidence of incentives being used by tobacco companies to make sure retailers stock certain products or stock products in a particular way. Further, it was clear that extra display features such as the hanging boxes and sample products behind RVM front panels functioned purely as advertising and had no practical use. In fact, one respondent reported having recently taken a hanging box down as it ‘got in the way’.

In conclusion, we would suggest that this study adds to the evidence that tobacco industry involvement and control in the retail space is significant and entrenched. The range of techniques the tobacco companies use (both in their relationships with individual retailers and in the retail press) fits with a model of push promotion through financial investment, coercion and incentives. This highlights the importance of the retail space as a promotional environment for tobacco, where the product is clearly being promoted and the industry is investing in a wide range of methods to maximise this promotional opportunity. The heavy involvement of the industry, the presence of a significant minority of RVMs and indications that retailers are being recruited away from traditional gantries to RVMs, indicate that implementation of PoS restrictions in England may mirror what has happened in Ireland. Beyond this, the standardised nature of gantries in England (if we do not see the expected shift to RVMs) is likely to make implementation low cost.

What this paper adds

Previous research has described tobacco promotion at the point of sale in a variety of jurisdictions under a range of regulatory frameworks. We examined promotional practices in two English cities operating under a partial restriction before a full prohibition of product display.

Retailers describe a relationship where manufacturers compete to exert control over the retail environment through a mixture of contractual obligations, incentives and pressure from company representatives.

There is evidence of the emergence of the retail vending machine, a new phenomenon in UK retail, which cedes any remaining control over product display from the retailer to the manufacturer.

Acknowledgments

The authors acknowledge the contribution of images provided by Jane MacGregor.

References

Footnotes

Funding No grant or other funding was obtained to support this research.

Competing interests Data were collected in the summer of 2009 during the passage through the UK Parliament of the Health Act (2009), which proposed powers to prohibit point-of-sale displays of tobacco products in England, Wales and Northern Ireland. Action on Smoking and Health (ASH), the employer of four of the co-authors is a member of the Smokefree Action Coalition, a network of over 70 health organisations advocating in support of the bill.

Provenance and peer review Not commissioned; externally peer reviewed.

↵i New South Wales, Australian Capital Territory and Western Australia by the end of 2010 (except tobacconists in NSW), and Victoria and Tasmania by early 2011.

↵ii Comparable figures are not available for the UK as, unlike the US government, in the UK the tobacco industry is not obliged to disclose what it spends on marketing and how this money is spent.

↵iii Which is now wholly owned by Japan Tobacco International.