Article Text

Abstract

Objective Originator pharmaceutical companies prolonging the patent of a medicine prevents rivals’ entry to the market and competition. As the entry of generic alternatives usually results in price reduction, any delay in their entry potentially deprives the National Health Service (NHS) of much-needed savings. This study estimates the potential cost savings lost to the NHS as a result of delayed entry of generic low-dose buprenorphine (LDTB) patches in England.

Design Two case scenarios were modelled to determine the savings from the entry of generic LDTB Butec only between February and August 2016 and the potential savings which could have been achieved if all generic LDTB patches had entered the market at the same time.

Setting The volume of utilisation of branded and generic LDTB in UK primary care was derived from the NHS business services authority website for prescriptions dispensed between February 2015 and January 2018.

Main outcome measures Cost savings associated with the entry of generic LDTB.

Results The cumulative cost savings from the introduction of Butec alone was £0.7 ($0.92) million. The model predicted that if all generic buprenorphine entered the market at the same time with Butec, they could have been achieved a £1.2 ($1.57) million saving. This means that approximately £0.5 ($0.65) million savings was lost to the NHS over the 6-month time period.

Conclusions The entry of Butec was associated with cost savings. We estimated that more cost savings could have been achieved if other generic LDTB patches had entered the market at the same time to drive competition between rivals. Patent protection strategies which delayed the entry of multiple generics were responsible for the reduced cost savings to the NHS in England.

- buprenorphine

- patent

- evergreening

- budget impact

- utilisation

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

Strengths and limitations of this study

The case scenarios were based on perspective (real) data and market reaction to the entry of generic medicines.

National Health Service business services authority website provides a reliable source for prescriptions dispensed in England.

Segmented regression of an interrupted time series is regarded as the gold standard in pharmacoepidemiological studies in such studies.

The case scenario 2 assumed that the market share of generics would behave in a similar way to Butec in scenario 1.

It is possible that the market share of the various products may have reacted differently with the availability of multiple generics in February 2016.

Introduction

According to the British Pain Society, 43% of the UK population are living with chronic pain that has lasted for 3 months or longer.1 2 Chronic pain prevalence increases with age to affect over 70% of individuals aged over 65-year-old, mainly due to arthritis or low back pain.2 3 Patients with chronic pain seek medical attention in primary care up to five times more frequently than others, which equates to almost five million primary care appointments a year.4

Low-dose transdermal buprenorphine (LDTB) patches are an established and cost-effective way of managing chronic pain unresponsive to oral analgesics and requires continuous release analgesics.3 5

Napp pharmaceuticals have held UK patent for the low-dose transdermal controlled release buprenorphine ‘BuTrans’ since 2005.6 In February 2016, this patent expired, and the company launched Butec, an identical version of BuTrans that differed only in name and priced competitively in 15% less than BuTrans price. At the same time, a competitor company (Sandoz) obtained market authorisation to launch a generic version of LDTB patches (Reletrans).6 The originator company claimed to the UK patents court a breach of patent on the basis that the patent ‘defines a transdermal patch comprising of 10% weight buprenorphine base; 10%–15% wt levulinic acid and ~10% weight oleyloleate as ingredients in the patches’ manufacture and that it would be difficult to determine output values especially since transdermal systems degraded over time’. This claim prevented the launch to market of all other generic LDTB patches. In August 2016, the Napp case went to appeal and judgement found in favour of Sandoz, allowing them to manufacture and market generic LDTB patches in competition with BuTrans and Butec patches in the UK.6 In September 2016, branded generic LDTB patches (non-originator products with a trade name produced by a manufacturer not the originator)7 such as Reletrans and Panitaz, and non-branded generic LDTB patches were launched and thus the market for LDTB changed.

The selection of a medication is largely dependent on key players in drug therapy decision-makings’ (physicians, clinical pharmacists and formulary committee members) prescribing behaviour. Studies have found that prescribing behaviour of prescribers are influenced by drug relating factors such as efficacy, safety, administration and cost and policy-related factors such as medicine inclusion in formularies, prescribing restrictions and prescribing guidelines.8–14

At the point of use of healthcare services and pharmaceuticals, the English national health system is funded through general taxation, such as the UK National Health Service (NHS), there is always pressure to remain within budget and provide value for money for tax payers.15 The UK exhibits one of the highest prices for branded products and the lowest prices for generics in Europe. In UK, the key bases of competition are product portfolio, competitive pricing, customer service and marketing strategy. Pricing has always been a key competitive tool.16

Generics remain a key element in government strategy for the cost-effective provision of medicines through the NHS.16 17 Generic prescribing is a standard practice in UK. Several factors have led to this practice, accounted for 81% of items prescribed in primary care in England and helped to achieve £7.1 billion savings since 1976 and allowed 490 million more items to be prescribed without an increase in total spending.18 19 INN prescribing is encouraged at early stages as medical schools in the UK are teaching medical students generic prescribing.20 Another factor is that physicians are encouraged in various ways, using both financial and non-financial incentives, to prescribe generics (using non-proprietary names), since this means community pharmacists dispensing general practitioners prescriptions are reimbursed at the lowest national drug tariff cost. Financial incentives include, for example, physicians’ budgets and budgetary incentives, generic prescribing targets with incentives. In budgetary incentives, savings achieved by the physicians beyond the indicative budget can be used for other purposes such as training. Other factors include empowering physicians with technology and decision support systems to help them prescribe generically (such as generic prescribing programmes) and providing them with information via national and local cost effective prescribing guidelines (eg, NICE guidelines). In addition, prescribing monitoring and feedback to improve physicians’ prescribing and awareness of medicines costs is also used to encourage generic prescribing.17 20 21

The aim of this paper is to understand the impact of the 6 months delay in the entry of multiple generic LDTB patches on the utilisation of LDTB patches in England and estimate any potential savings lost to the NHS.

Method

Data source

The study was a retrospective analysis of the utilisation of LDTB patches in primary care in England. Primary care data on the monthly volume and net ingredient cost of medicines were derived from the NHS business services authority (NHSBSA) website for prescriptions dispensed between February 2015 and January 2018.22 This website (database) captured monthly information (drug name, dose, quantity, drug tariff price and the total cost) on all medicines dispensed by community pharmacies against prescriptions issued by general medical practitioners and non-medical prescribers (nurses and pharmacists) in England. Primary care prices were the drug tariff prices, which were the prices that set out by the department of health and social care on what pharmacies would be reimbursed for the cost of each generic medicine they dispense for an NHS prescription (before discounts and not including dispensing costs), excluding value-added tax since medicines supplied against primary care prescriptions in the UK are exempt from value-added tax. Two case scenarios were modelled, to determine the savings from the entry of Butec only between February and August 2016, and the potential savings which could have been achieved if all generic LDTB patches had entered the market at the same time. The average costs per mg of different LDTB patches and the estimated savings in analysis are presented in British pounds and US dollars using historical average annual exchange rates corresponding to each year in the study (in 2015 £1=$1.51, 2016–2018 1£=$1.31).23

Statistical analysis

Average costs per mg of LDTB

Due to the non-uniform linear price change per mg between all strengths of LDTB patches, and the 5 mcg/hour strength patches was the most frequently prescribed strength rather than the 10, 15 and 20 mcg/hour strengths, we chose the cost of this strength to determine the average cost/mg of LDTB (table 1).

Average costs per mg in sterling pounds and US dollars of 5 mcg/hour transdermal buprenorphine patches in primary care in England between 2015 and 2018

Case 1: Savings from the entry of Butec only

Monthly usage and expenditure on BuTrans and Butec between February and August 2016 were taken from the NHSBSA website. This total usage was then multiplied by the price of BuTrans over the same period (since the price of BuTrans did not change before or after the introduction of Butec) to calculate what the expenditure would have been without the introduction of Butec. The actual cost for both BuTrans and Butec over this period was then deducted from this estimated expenditure to calculate the actual savings to the NHS as a result of the entry of Butec.

Case 2: Forecasted savings if all generic LDTB patches had entered the market in February 2016

To estimate the savings that could have been achieved if other generic LDTB patches (Reletrans, Panitaz and non-branded generic buprenorphine) had entered the market at the same time as Butec, a model was built, based on generic LDTB market shares. It was assumed that the total market shares of these other LDTB patches would have changed as for Butec’s entry in 2016, that is, 1% in February and March, 2% in April, 8% in May, 17% in June, 27% in July and 38% in August. In this model, the utilisation of each generic was multiplied by their actual price in September 2016 to calculate the hypothetical expenditure during the period February to August 2016. This hypothetical expenditure was then deducted from the LDTB patches expenditure in the BuTrans only scenario (from Case 1) to calculate the potential savings that may have been achieved from the entry of all generics at the same time as Butec (Case 2). This hypothetical saving (Case 2) was then deducted from the actual savings from the entry of Butec (Case 1) to calculate the savings lost from the delayed entry of these branded generics.

Linear regression

Overall expenditure and utilisation trends were examined for LDTB patches in primary care over the period February 2015– January 2018. Linear regression analyses were used with a month as the independent variable and overall expenditure or utilisation in milligrams as the dependent variable. The regression coefficient values were divided by the baseline expenditure or utilisation (in February 2015) to calculate the average monthly percentage increase or decrease in expenditure or utilisation of LDTB patches.

Segmented regression

Segmented regression analysis of interrupted time series data was used to examine the impact of the launch of generic LDTB patches on the prescribing of the originator brand BuTrans and to establish when the gradient changed, using the method of Wagner et al.24 The effect was assessed by two parameters, level (β2 and β4) and trend (β3 and β5). The following segmented regression analysis equation was applied to each individual study outcome measure:

Yt = β0 + β1 * time + β2 * launch of Butec in February 2016 + β3 * time after launch of Butec in February 2016 + β4 * launch of generic LDTB other than Butec in September 2016 + β5 * time after launch of generic LDTB other than Butec in September 2016 + et

where Yt is the monthly outcome measure. Time was a continuous variable referring to time, in months, from the start of the observation period, ranging from 1 to 36 from the start to the end of the study period. The launch of Butec in February 2016 was a dichotomous variable (0 before February 2016; 1 since February 2016). Time after launch of Butec in February 2016 was a continuous variable beginning in February 2016. β0 and β1 represent the intercept and trend over time during the preintervention period, respectively. β2 represents the change in the level at the time of launch of Butec in February 2016 and β3 represents the trend change in the slope after launch of Butec in February 2016, both compared with those in the preintervention period. β4 represents the change in the level at the time of launch of generic LDTB other than Butec in September 2016 and β5 represents the trend change in the slope after launch of generic LDTB other than Butec in September 2016. et represents the error term. All calculations were performed using Microsoft Excel 2013 and STATA MP13.

Patient and public involvement

No patients or members of the public were involved in this study.

Results

Prices LDTB patches

Between February 2015 and July 2017, the prices of BuTrans (originator brand of LDTB) and non-branded generic buprenorphine were not changed. Butec patches price reduced gradually by 50% over the same time period. Prices of Reletrans and Panitaz decreased in a similar gradual manner. Post-August 2017, the prices of the majority of buprenorphine patches were increased (table 1).

Utilisation of LDTB patches

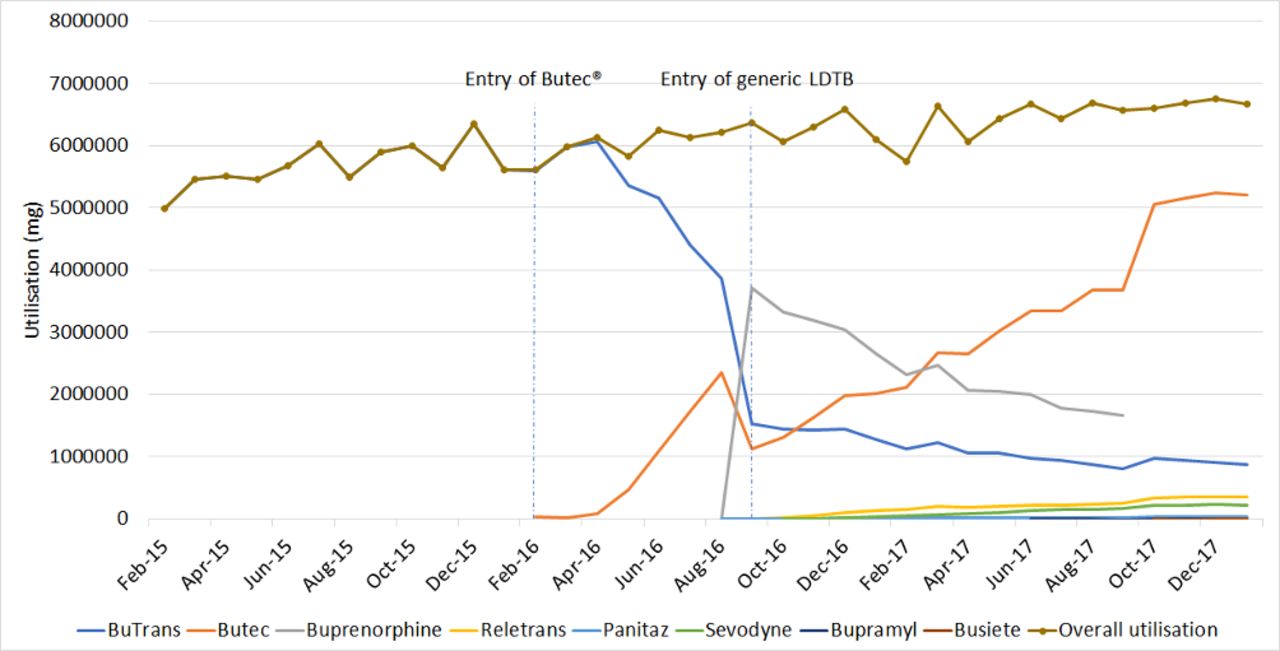

Regression analysis indicated that the overall utilisation of LDTB patches increased significantly (p>0.001) by an average of 4.8% per month (95% CI 4.2 to 5.4) from 4 981 900 mg in February 2015 to 6 668 540 mg in January 2018. Following the patent expiry of the brand BuTrans and the entry of the originator company own branded generic Butec in February 2016 and competitor companies’ generics Reletrans, Panitaz and non-branded generic buprenorphine (in September 2016), Sevodyne, Bupramyl and Busiete (in 2017), the market share of these agents changed dramatically. Butec started to gain market share although gradually between February and August 2016 and achieved 38% of the market by August 2016. In contrast, non-branded generic buprenorphine gained a high market share (58%) on entry in September 2016 (figure 1). Following an initial fall when competitor generics were launched in September 2016, the market share of Butec started to increase again and achieved 78% of the market by January 2018. The utilisation of BuTrans (originator brand) and non-branded generic buprenorphine fell during this period and the other generics gained little market share since launch (figure 1).

Utilisation of low-dose transdermal buprenorphine patches in England primary care between 2015 and 2018. LDTB, low-dose buprenorphine.

Expenditure on LDTB patches

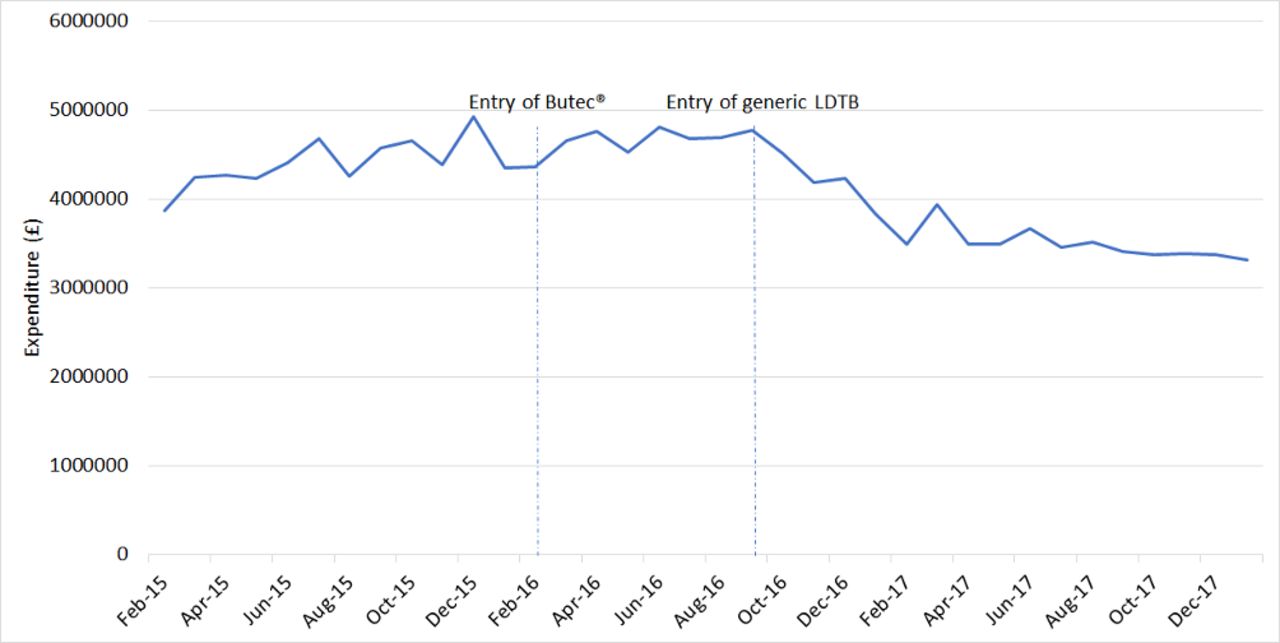

Regression analysis indicated that the overall monthly expenditure on LDTB patches decreased significantly (p>0.001) by an average of 1.11% per month (95% CI −0.82 to −1.71) from £3 868 890 ($5 859 836) in February 2015 to £3 321 780 ($4 327 013) in January 2018. Figure 2 shows that before September 2016, the overall primary care expenditure on LDTB patches follows the utilisation pattern. Post-September 2016, the expenditure decreased in spite of the increased utilisation of LDTB patches.

Expenditure on low-dose transdermal buprenorphine patches in England primary care between 2015 and 2018. LDTB, low-dose buprenorphine.

Segmented regression of interrupted time series

Pre-Butec entry market phase (February 2015–January 2016)

The trend of interrupted time series analysis (table 2) indicates that the monthly utilisation of the brand BuTrans rose significantly before the introduction of Butec in February 2016, as shown by the change in slope β1 (table 2).

Interrupted time series regression analysis of change in the utilisation of LDTB patches in England

Post-Butec entry market phase market phase (February 2016–August 2016)

The change in trend (β3) showed a statistically significant increase in utilisation of Butec patches and a significant negative impact on the utilisation of the brand BuTrans (table 2 and figure 1). The level (β2) of the brand BuTrans did not change significantly (table 2).

Post-other generic LDTB entry market phase market phase (September 2016–January 2018)

Once generic LDTB (other than Butec) were available, there was a significant decrease in the level of utilisation (β4) of BuTrans and Butec. The trend of utilisation (β5) of BuTrans and non-branded generic buprenorphine decreased significantly during this phase. In contrast, the trend of utilisation of Butec, Reletrans, Panitaz, Sevodyne Bupramyl and Busiete increased during this phase.

The change in the trend was significant for Butec, Reletrans, Panitaz and Sevodyne, although the actual utilisation of the later three generics were relatively low compared with Butec (table 2 and figure 1).

Table 3 shows that between February and August 2016, when Butec was the only branded generic LDTB in the market, there was a saving of £705 917 ($924 751) in primary care in England.

Expected, actual and hypothetical savings from the entry of generic LDTB patches

A hypothetical model (figure 3) was built to simulate the entry of all generic LDTB at the same time, between February and August 2016, to determine the potential savings that could have been achieved if they had all entered the market in February 2016. Table 3 shows that if all generic LDTB patches had entered the market at the same time with Butec, savings of £1 202 132 ($1 574 792) could have been achieved. This represents a further £0.5 ($0.655) million savings that was lost to the NHS over this 6-month period.

{kind=link}

{kind=link}

{kind=link}

Hypothetical model for the market share if all generic LDTB entered in February 2016. LDTB, low-dose buprenorphine.

Discussion

In 2016/2017, the NHS spent £15.4 billion on medicines in both primary and secondary care; only 28% of this expenditure was on generic medicines.19 The pharmaceutical market is lucrative and competitive, and the introduction of generic alternatives poses a financial threat to the branded drug industry. The market share of branded medicines is protected via patent.25 At the time of patent expiration, innovator firms often attempt to extend the patent life of their products, to maintain market exclusivity and avoid losing profit. Several strategies have been used to combat generic competition, including changing the dosage form, modified release formulation, combination products, alteration to the next generation of metabolites or analogues or extending licensed indication, so-called ‘evergreening’ strategies.26–30 A more recent method of protecting market share is for innovator firms to acquire generics operations or produce their own generics, often known as ‘flanking generics’.25 This strategy enables the entry of a generic version to the market without any loss in the market share, making the market less attractive to the entry of other rivals, since they would have to compete with greater discounts to make their product attractive. Napp appears to employed such a strategy by launching their own generic first and then appealed an infringement of its patent by Sandoz in the UK patent court, thus delaying entry of other competitors.6

This study aimed to understand the impact of the delayed the entry of generic LDTB patches in England. Our study is the first to calculate the impact of delayed entry of generic LDTB patches other than Butec and estimating the potential savings lost to the NHS realised from this delay in England.

Two different pricing strategies appeared to have been implemented by the innovator company following the launch of ‘Butec’. With the higher unit price of the originator brand, BuTrans, was unchanged to maintain revenue through brand loyalty. The branded generic, Butec, was originally discounted by 15% compared with BuTrans. Once the patent case was successfully appealed and other generic LDTB entered the market, the price fell sharply to 50% of the originator brand and matched the price of the newly launched generics (table 1). The time of entry of Butec as a first generic LDTB, being identical to the originator brand (BuTrans) and its lower price were responsible for the innovator company retaining 91% of the market.

Market genericisation and the price reduction due to competition for market share between these were responsible for the significant reduction in the overall expenditure on LDTB in England primary care despite the significant increase in the utilisation (figure 2).

Segmented regression analysis was used to identify the impact of marketing of Butec and other generic LDTB on the prescribing of the brand originator BuTrans and the impact of the marketing of Butec on the utilisation of other generic LDTB in primary care in England. Before the patent expiry of BuTrans and the entry of Butec, the utilisation of BuTrans was increasing significantly (table 2). The slow market growth of Butec during the first 3 months of entry was responsible for non-significant change in the level of utilisation of BuTrans (table 2). After this lag period, Butec started to replace BuTrans in the market, as the trend of utilisation of Butec exceeded BuTrans trend. This lag period might be due to the time it took for Butec to be included in the clinical commissioning group (CCG) formularies and prescribing software such as EMIS, as well as the time for awareness among prescribers to the availability of Butec.

Once other generic LDTB patches were available, other than Butec, the only generic to gain market traction was non-branded generic buprenorphine, which achieved 58% of the market at the time of entry. Since LDTB was eligible for automatic substitution in primary care, therefore, when LDTB prescribed generically or by non-proprietary name, it is possible that the non-branded generic buprenorphine may have been dispensed. Interestingly, a similar situation has been reported with pregabalin during a period of patent litigation between 2015 and 2017, in which the generic pregabalin did not result in cost savings to the NHS, despite gaining more than half of the market. This is due to the reimbursement price for this generic being similar to the brand Lyrica.31 Smyth et al 32 suggested that the generic pregabalin was priced in this way, because the UK Department of Health did not wish to recategorise pregabalin as generic while the originator brand Lyrica second patent (pain patent) was still being asserted by Pfizer.32 This introduction of generic LDTB (other than Butec) was responsible for an immediate decline in the level of utilisation of BuTrans and Butec (table 2).

The price flexibility strategy adopted for Butec was probably responsible for the recovery in the uptake of this product and the decline in the utilisation of non-branded generic buprenorphine where a price did not change in response to the competition (table 1). In October 2017, the Care Quality Commission recommended that buprenorphine patches should be prescribed by brand name rather than by non-proprietary name, to avoid any confusion due to the high incidence of actual harm from buprenorphine transdermal patches.33 34 At the same time, the non-branded generic buprenorphine was withdrawn from the UK market. Butec captured a significant market share and helped the company to retain 91% of LDTB patches market. This market share was then maintained with the Care Quality Commission recommendation to prescribe by brand name. In addition to price flexibility strategy, prescriber and commissioner familiarity with Butec as the only generic LDTB patch available from February to August 2016, may also have contributed to this gain in market share. For example, a number of CCGs such as Calderdale, Greater Glasgow and Clyde, Hambleton, Richmondshire and Whitby, Oxfordshire, Sheffield and Sunderland Medicines Optimisation Group recommended Butec as a brand of choice of LDTB patches in primary care, replacing BuTrans since it is identical in formulation to BuTrans and strength (5, 10, 15 and 20 mcg/hr) and also lower in price, thus offering significant savings.35–40

Two case scenarios were modelled, to determine the savings from the entry of Butec only between February and August 2016, and the potential savings which could have been achieved if all generic LDTB patches had entered the market at the same time.

The results of these models showed that the introduction of all generics LDTB at the same time of Butec could have delivered a higher cost saving to the NHS (£1.2 ($1.57) million) compared with (£0.7 ($0.92) million) as a result of the entry of Butec alone (table 3). These lost savings to the NHS are funds wasted directly impacting patients and ultimately tax payers which could be reinvested in other services for the patients. Previous work has established that when all other factors are equal, price strongly influences prescribing.41 42 Thus, as Butec was identical to BuTrans in all but name (manufactured on the same line and so on), then it was an attractive, less expensive alternative to BuTrans. Although about £0.5 ($0.65) million in potential savings was lost to the NHS, the savings lost were unlikely to have been greater as the strategy of increased price reduction of Butec, which occurred at the entry of generic competitors, would most likely have occurred earlier and still restricted the market growth of competitor generics. The lost savings from the delayed entry of generic LDTB patches is much less than savings lost from the prolongation of the patent of Lyrica, which has been estimated to be approximately £500 million due to the longer duration of litigation and greater utilisation of pregabalin in comparison with LDTB patches.29 Our study and the work done by Croker et al support the estimate that a more cost effective policy could save the NHS over £1 billion per year.31 43

The LDTB market did not behave as would be expected following patent expiry and introduction of generics. For example, following the patent expiry of atorvastatin in 2011, the price of the brand (Lipitor) decreased by 50% and generic atorvastatin were priced at 25% of this brand price, which resulted in significant cost savings to the NHS.30 In the case of LDTB patches, the legal challenge by the innovator company resulted in a 6-month delay in the launch of competitor generics. This delay allowed the innovator own generic to gain significant market share which was subsequently maintained when other competitor generics launched 6 months later. Our model suggests that the 6-month delay resulted in a potential £0.5 ($0.65) million worth of savings being lost to the NHS. It is unlikely that the NHS has lost significantly more savings due to the late entry of all generic LDTB patches since their introduction has resulted in the manufacturer of leading generic LDTB patch, Butec, to reduce its price significantly. Our results are in line with Duerden and Hughes study results that suggested that switching to generics are dependent on the availability and timing of introduction of generic products.20

Our study has some limitations. The model built did not consider the impact of the entry of multiple generics on the market share and the price of the originator brand, since the entry of large number of generics (ie, competitors) would be expected to be associated with a sharp price reduction and/or market share of the originator brand. In the case of LDTB patches, this impact was prevented by the originator company producing its own generic and delaying the entry of competitor generics. Furthermore, the prices used in this analysis were the standard list prices of the drug and not including dispensing costs. The savings listed and relative costings are based on net ingredient cost, but the average discount deduction made to chemist contractors of approximately 8% may mean that the actual costs are different. The case scenario two assumed that the market share of generics would behave in a similar way to Butec in scenario 1. It is possible that the market share of the various products may have reacted differently with the availability of multiple generics in February 2016. A non-uniform linear price change per mg between all strengths of the patches exists, therefore, the average cost per mg for the most frequently prescribed strength was chosen.

Conclusion

The entry of Butec following the patent expiry of BuTrans was associated with apparent cost saving. More cost savings could have been achieved if other generic LDTB entered the market at the same time to drive competition between rivals. Patent protection strategies which delayed the entry of multiple generics was responsible for the reduced cost savings to the NHS in England but later minimised by an aggressive price reduction strategy.

References

Footnotes

Contributors All authors have contributed to this study and all authors reviewed and approved the final version of the manuscript. SRC designed the study, interpreted the results and reviewed the manuscript and corrected the final version of the manuscript. MIA participated in the study design, data collection and interpretation of results, prepared the manuscript draft and performed all analytical testing and manuscript review. RWF participated in the study design, interpreted the results and reviewed the manuscript and corrected the final version of the manuscript.

Funding This research was not funded or sponsored by any organisation and the researchers are independent of any funding bodies.

Competing interests None declared.

Provenance and peer review Not commissioned; externally peer reviewed.

Data sharing statement Data collected from survey are anonymised. The raw data from which result paper are derived can be made available on request.

Author note Access to data: All authors had full access to all of the data (including statistical reports and tables) in the study and can take responsibility for the integrity of the data and the accuracy of the data analysis.