Article Text

Abstract

Objectives This study aims to assess the impact of the subsidised community health insurance scheme in Senegal particularly on the poor.

Design and setting The study used data from a household survey conducted in 2019 in three regions, representing 29.3% of the total population. Inverse probability of treatment weighting approach was applied for the analysis.

Participants 1766 households with 15 584 individuals selected through a stratified random sampling with two draws.

Main outcome measures The impact of community-based health insurance (CBHI) was evaluated on poor people’s access to care and on their financial protection. For the measurement of access to care, we were interested in the use of health services and non-withdrawal from care in case of illness. To assess financial protection, we looked at out-of-pocket expenditure by type of provider and by type of service, the weight of out-of-pocket expenditure on household income, non-exposure to impoverishing health expenditure and non-exposure to catastrophic health expenditure.

Results The results indicate that the CBHI increases primary healthcare utilisation for non-poor (OR 1.36 (CI90 1.02–1.8) for the general scheme and 1.37 (CI90 1.06–1.77) for the special scheme for indigent recipients of social cash transfers), protect them against catastrophic (OR 1.63 (CI90 1.12–2.39)) or impoverishing (OR 2.4 (CI90 1.27–4.5)) health expenditures. However, CBHI has no impact on the poor’s healthcare utilisation (OR 0.61 (CI90 0.4–0.94)) and do not protect them from the burden related to healthcare expenditures (OR: 0.27 (CI90 0.13–0.54)).

Conclusion Our study found that CBHI has an impact on the non-poor but does not sufficiently protect the poor. This leads us to conclude that a health insurance programme designed for the general population may not be appropriate for the poor. A qualitative study should be conducted to better understand the non-financial barriers to accessing care that may disproportionately affect the poorest.

- public health

- health economics

- health policy

- health economics

Data availability statement

Data are available on reasonable request. Data are available on reasonable request. The study data are not available in a repository, but sharing will be considered by request.

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

STRENGTHS AND LIMITATIONS OF THIS STUDY

The subgroup analysis was conducted using a method that ensures balance in both the total sample and the subgroups.

The impact of the insurance schemes was measured on both financial protection and care utilisation.

Because of the small number of insured in the sample, the control group is 28 times larger than the treatment groups.

We had to reduce the CI to 90% in order to have maximum significant results

Introduction

The Senegalese government introduced compulsory health insurance for civil servants and workers in the formal private sector from the early 1970s.1 However, in an environment dominated by informal activity, the proportion of the population covered remained very low for a long time.2 This has had an unfavourable impact on healthcare utilisation and on the burden of healthcare costs supported by households.3 This is why, in 2013, the government set up a programme to generalise health insurance4 called Couverture Maladie Universelle (CMU). Its main component is a community-based health insurance (CBHI) scheme that includes a general scheme (CBHI-1), partially subsidised, and a special scheme for the poor (CBHI-2), fully financed by the state (registration and free care).4 As in some other African countries,5–7 this special health insurance scheme for the poor is backed by the public cash transfer programme for the poor initiated with World Bank support. Thus, members of households benefiting from the national family financial-security grant programme (Programme national de Bourses de Sécurité Familiale or PNBSF) are enrolled in the insurance scheme for the poor. CBHI-1 is a voluntary scheme, open to all. The annual contribution is CFA7000 (about US$10). It guarantees insured persons 80% coverage of most services offered by public health facilities and 50% coverage of private pharmacy drugs. The enrolment of CBHI-2 beneficiaries in mutual health insurance schemes is, in principle, fully subsidised by the Senegalese Agency for universal health coverage (UHC). These beneficiaries are normally covered at 100% by CBHI.

Before starting the CMU programme, CBHI was presented by the Senegalese health authorities as a mechanism that could encourage the use of health services and promote the financial protection of the population, particularly the poorest,8 although a growing amount of literature on the impact of CBHI in Africa has produced mixed results. Indeed, while some studies have shown that CBHI can facilitate and encourage access to care,9–14 particularly for outpatient care,15 16 skilled maternal and child healthcare17–27 and drugs,28 other studies have found the opposite for prenatal care,26 preventive health services12 and hospital care.15 In line with this second trend, it was found in Rwanda11 and Burkina Faso15 that very poor individuals, once insured, were less likely to use health services than the non-poor. In terms of financial protection, studies have shown that membership in CBHI schemes can reduce healthcare expenditures,9 29 30 especially expenditures on outpatient care.16 It can also reduce exposure to catastrophic health expenditures,11 14 29 31 especially for the poorest.30 Similarly, in Mali,10 a 2008 study showed that CBHI provide protection against catastrophic health expenditure related to hospitalisation. However, in contrast to these findings, other studies have shown that CBHI is not protective in each situation. In Tanzania12 and Burkina Faso,31 they did not have a significant impact on reducing healthcare spending. In Mali, this lack of significant effect was observed on ambulatory care expenditure.10 In Rwanda, insured people in the poorest expenditure quintile had a higher rate of catastrophic health expenditure than the rest of the population.11

The same mixed findings on the impact of CBHI have been reported in Senegal by Jutting,32 Chankova, Sulzbach and Diop,10 and Smith and Sulzbach.27 These impact evaluations showed that CBHI had a positive effect on access to hospitalisation,10 32 on the use of assisted delivery by health professionals,27 and on the reduction of delivery and hospitalisation expenses.10 32 In contrast, it did not appear to be contributing significantly to the use of ambulatory services10 and access to prenatal care.27 Similarly, there was no protective effect on out-of-pocket spending on ambulatory care.10

These three studies,10 27 32 which are the only ones to have tried to evaluate the impact of CBHI in Senegal, predate the subsidised CBHI programme, which means that there is still no published research on the impact of CBHI of the CMU programme in Senegal. It is important to measure the effects of this strategy in order to correct its implementation if necessary and, furthermore, to contribute to the growing debate on the relevance of CBHI in Africa.33–37

The purpose of this study is to measure the effect of the two CBHI schemes (a partially subsidised general scheme—CBHI 1—and a fully subsidised scheme dedicated to beneficiaries of the PNBSF-CBHI 2). We were particularly interested in the poorest people. These are those who live in households with a consumption level below the national poverty line.38 39 Thus, by comparing poor members of CBHI with different control groups, after inverse probability of treatment weighting (IPTW—see in the Method section), we attempt to verify whether subsidised CBHI guarantee poor people greater access to care and adequate financial protection. Many impact studies on CBHI in Africa focus on one or the other of these dimensions of UHC,9 13 15 17 18 20–26 28–30 40 41 but rarely on both.11 12 14 16 31 42 However, as Wagstaff et al43 have pointed out, the two dimensions of UHC must be examined together because good performance on one aspect is no guarantee of overall performance. A low incidence of catastrophic health expenditure may mean that people do not receive care and therefore do not spend on it. Similarly, high healthcare utilisation among the insured in a voluntary system may not be related to insurance performance but rather to the existence of strong adverse selection, that is, sick people are more likely to buy insurance while healthier people buy less.44 For all these reasons, it is recommended that the two dimensions of UHC be assessed together. This is what we intend to do in this paper, with a particular focus on the poor.

Method

Data

The data for this study come from a household survey conducted in early 2019 in the regions of Diourbel, Thiès and Tambacounda. These regions account for 29.3% of the total population of Senegal. Households were selected through a stratified random sampling with two draws. The regions constitute the strata and the census districts the clusters. The first draw selected 176 clusters within the three strata. The probability of selection of each district was proportional to its size. The second draw consisted of randomly selecting 12 households within each cluster. The goal is to survey 10 households per cluster. However, 2 additional households were selected in case of refusal among the first 10 households. For the selection of households, a sampling interval or sampling step p is determined. Then, a number k between 1 and p is randomly drawn and incremented by adding p each time, to find the 10 households and the two replacements. In total, the survey involved 1766 households with 15 584 individuals. In each of the 176 clusters, there were at least 10 households that responded. The questionnaire included items on household and individual sociodemographic characteristics, health, health insurance, consumption, savings and housing, among others.39 45

Variables of interest

The impact of CMU schemes was assessed based on healthcare utilisation and on financial protection of poor people. For the measurement of access to care, we were interested in the use of health services and the foregoing of care when sick. Forgoing care occurs if a person has been ill but has not used care. Utilisation is first measured globally, taking all services and providers together, and then in detail, by service consumed and by type of provider (consultations and outpatient care, hospitalisation, drugs, health posts, health centres and public hospitals).

To assess financial protection, we looked at out-of-pocket expenditure by type of provider and by type of service, the weight of out-of-pocket expenditure on household income, non-exposure to impoverishing health expenditure and non-exposure to catastrophic health expenditure according to the three thresholds most commonly used in the literature.46 These are the thresholds used by the Sustainable Development Goals, that is, 10% (threshold 1) and 25% (threshold 2) if health expenditure is related to total expenditure46; and the threshold of 40% (threshold 3) set by the WHO if out-of-pocket expenditure are related to non-subsistence expenditure.47

The construction of the financial protection variables and the identification of the poor required an estimation of the monthly resources of the households included in the survey45 and the determination of the monthly poverty line. For the estimation of resources, it is generally accepted that, given the difficulty of determining incomes with sufficient accuracy in low-income and middle-income countries, household consumption expenditure is a good measurement tool that takes into account income of all kinds as well as savings.43 46 We constructed this aggregate of household consumption by summing food and non-food expenditures. For food consumption, the variable includes the standardised monetary value of products purchased, the value of meals eaten outside the household, the estimate of self-consumption and, more globally, of non-monetary food consumption (meals offered, eg). The non-food consumption variable aggregates the use value of durable goods, the use value of non-durable goods, non-food expenditures incurred during the holidays and services consumed. Health expenditures are included in this category. For the determination of the poverty line, we used the median level of food expenditure in the population, estimated here as the average food expenditure of households located between the 45th and 55th percentiles.38 Payment capacity is equal to non-subsistence expenditure.38 This is the difference between total expenditure and food expenditure or between total expenditure and subsistence expenditure, if the latter is greater than food expenditure.38 Subsistence expenditures are obtained by multiplying the poverty line by the standardised household size.38 This is intended to allow comparison between households, which would eliminate differences in the age and gender of household members.48 Various equivalence scales have been proposed in the literature.39 For the purposes of this study, we have selected one of the scales used by the Senegalese statistics agency and also used by other African countries.39 48 It is shown in table 1.

Age and gender equivalence scales for household size standardisation

Method of analysis

After identifying the poor and non-poor and constructing the different variables to compare, we went on to estimate the impact of the two CBHI schemes by IPTW.49 50 It is a method based on the propensity score, a statistical tool that makes it possible to mimic the operation of a randomised controlled trial by creating, in a non-experimental context, a fairly comparable treatment group (programme beneficiaries) and control group (non-beneficiaries).50 To be reliable, the propensity score must be calculated using all the confounding variables. Indeed, it is necessary to ensure a balanced distribution between the different groups of all potentially confounding factors, that is, individual characteristics that may influence the measured effect.51

Inverse weighting is one of the four quasi-experimental methods of impact assessment, along with matching, stratification and adjustment.52 Everyone is given a weight equal to the inverse of the probability of receiving the treatment. Since the propensity score is the probability of receiving the treatment, the weights of the treatment group are weighted by 1/SP, and those of the control group by 1/(1-SP).52

In our study, we set up three comparison groups: a control group composed of individuals not enrolled in a CBHI scheme and two groups composed of the respective beneficiaries of each of the two CBHI schemes. A comparison of the means and proportions in the three groups was then made after weighting on the propensity score of the different subjects.

The propensity score was determined here using a multivariate probit model. In order to reduce bias related to confounding factors that may influence healthcare utilisation or promote financial protection in health, we rebalanced the groups using the variables that we felt could affect these outcomes of interest.51 These variables are as follows: occupation (working or not), age group (less than 5 years, 5–14 years, 15–44 years, 45–59 years, more than 60 years old), religion, gender, education level, Quranic schooling, enrolment in another insurance scheme (private insurance, free healthcare, civil servants' insurance and private sector insurance), the main pathology reported in the 3 months preceding the survey, the relationship with the head of the household (belongs to the nuclear family of the head of the household or not), the size of the household (household size less than or equal to the national average or not) and whether or not the household is poor. All these variables were dichotomised, resulting in 47 different variables for propensity score calculation.

Once the propensity scores were estimated, we used them for weighted balancing of the poor and non-poor subgroups and the total population.53 54 All 47 variables showed a difference in standardised means after balancing that was below the recommended 10% threshold.49 Moreover, 46 variables were balanced at the 5% threshold. Finally, after balancing, we estimated the effect of the general and special insurance schemes using generalised linear regression.

All analyses were performed with R software and the WeightIt package for propensity score weighting, Survey for estimation of binomial effects and SvyVGAM for multinomial effects.

Patient and public involvement

Patients or the public were not involved in the design, or conduct, or reporting, or dissemination plans of our research.

Results

Socioeconomic characteristics of the study groups

Table 2 summarises the characteristics of the people surveyed and the data on healthcare utilisation and financial protection of the members of the different schemes. It reveals, among other things, that the insured of the general scheme (CBHI-1) and those of the special scheme (CBHI-2) constitute, respectively, 2.14% and 2.36% of the study population. The coverage rate of the second scheme is lower than expected. In principle, it should be 21.53%, which is the proportion of the sample composed of members of households benefiting from the PNBSF, all of whom are normally eligible for the poor insurance scheme.

Characteristics of insurance scheme members and non-members

The incidence of individual poverty is 21.9% among CBHI-1 members and 36.4% among CBHI-2 members. In the latter, it would normally be close to 100% because the PNBSF is targeted at the poorest households. However, measuring the poverty rate among the beneficiaries of this PNBSF shows that 56.9% of them do not belong to poor households (national poverty line).

Figure 1 shows the distribution of the different schemes within the wealth quintiles. The proportion of insured under the general contributory and voluntary scheme (CBHI-1) is higher in the two highest quintiles (3.2% and 2.73%). It is lower in the poorest quintile (1.12%).

Distribution of insured and uninsured by wealth quintile.

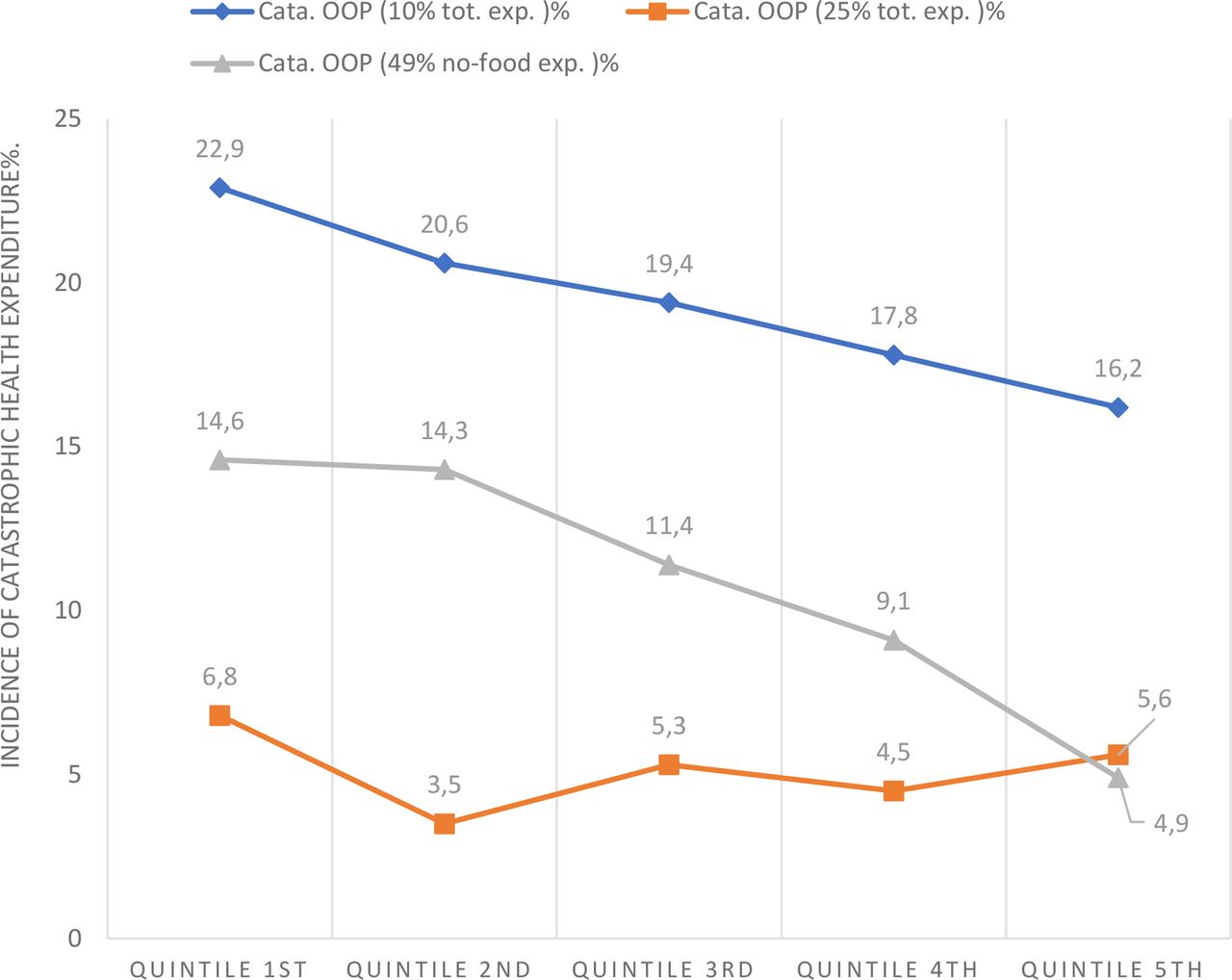

Incidence of catastrophic payments

The proportion of households facing catastrophic expenses is 19.4% (threshold 1), 5.1% (threshold 2) and 10.9% (threshold 3). Figure 2 compares the results by quintile. It shows that the incidence of catastrophic spending at threshold 1 (10% of total spending) and threshold 3 (40% of non-subsistence spending) decreases as income increases. In contrast, at threshold 2 (25% of total expenditures), catastrophic expenditures do not change with income. Quintile 1 (the poorest) has the highest proportion of individuals affected (6.8%), followed by quintiles 5, 3 and 4 (5.6%, 5.3% and 4.5%) and finally quintile 2 (3.5%).

{kind=link}

{kind=link}

Incidence rate of catastrophic payments by wealth quintile.OOP, Out of pocket.

Impact of CBHI schemes on healthcare utilisation and financial protection

Our regressions (see table 3) show that CBHI improves healthcare utilisation and financial protection in the population, regardless of the scheme considered. Insured people use care more frequently than non-insured people, both in the general scheme (CBHI 1- OR: 1.36; CI90 (1.02–1.8)) and in the special poor scheme (CBHI 2- OR: 1.37; CI90 (1.06–1.77)). CBHI-1 protects its beneficiaries from catastrophic health spending at the 10% threshold (OR: 1.63; CI90 (1.12–2.39)) and CBHI-2 does the same at the 25% threshold (OR: 3.06; CI90 (1.24–7.56)), as well as protecting against impoverishing out-of-pocket expenditure (OR: 2.4; CI90 (1.27–4.5)). When they are ill, members of the general scheme (CBHI-1) forego care less often than the non-insured (OR: 2.23; CI90 (1.18–4.21)). Those in the special scheme (CBHI-2) incur lower expenses in proportion to household income than the uninsured (estimate: −0.02; CI90 (−0.03–−0.01)).

Estimated effects of CBHI by scheme and poverty status

Conversely, CBHI has no positive effect on insured persons belonging to households below the poverty line. The probability of accessing care (OR: 0.61; CI90 (0.4–0.94)) or not foregoing care in the event of illness (OR: 0.41; CI90 (0.19–0.89)) is lower for the latter if they are covered by CBHI-2. The CBHI-1 results, although statistically insignificant on these variables, also show that insured poor people are less likely to use care (OR: 0.58; CI90 (0.32–1.04)) or not to forego care in case of illness (OR: 0.8; CI90 (0.27–2.34)). Moreover, for poor members of CBHI in both schemes, the proportion of out-of-pocket expenditure to household income tends to increase and, more importantly, they are less protected against catastrophic health expenditures at both the 10% (for CBHI-1, OR: 0.27; CI90 (0.13–0.54); for CBHI-2, OR: 0.5; CI90 (0.3; 0.83)) and 25% (for CBHI-1, OR: 0.44; CI90 (0.2–0.97)) levels.

Discussion

The results of our study show that subsidised CBHI has a different effect on the non-poor than on the poor. For the non-poor, it increases the likelihood of accessing care, reduces the risk of foregoing care, reduces out-of-pocket expenditure and protects against catastrophic or impoverishing expenditures. These results are consistent with those of similar studies conducted in other African countries, which found that CBHI had a significant impact on healthcare utilisation,9–14 on the reduction of health expenditures9 12 16 29 30 and on protection against catastrophic health expenditures.10 11 14 29 31

In contrast, for the poor, our study shows that CBHI has no impact on access to care, on foregoing care, on reducing out-of-pocket expenditure and on catastrophic health expenditure. Even the special poor scheme (CBHI-2), which in theory provides full coverage (there are no premiums or co-payments), does not produce better outcomes than the general scheme (CBHI-1). This result is in line with studies that show that CBHI schemes do not remove all barriers to access to healthcare, whether financial (eg, transport costs) or non-financial.55 This also confirms that UHC policies in low-income and middle-income countries can exacerbate the gaps between the poor and the non-poor.56–58 Correcting this lack of equity requires a redefinition of these policies and a better consideration of all dimensions of equity.59

We have also shown that CBHI does not improve healthcare utilisation for the poor or provide them with sufficient financial protection. Research in Rwanda,11 Tanzania12 and Burkina Faso15 31 has come to similar conclusions, finding that the very poor, despite CBHI, are less likely to use health services, face higher out-of-pocket expenditure or have higher rates of catastrophic health expenditures than the rest of the population. This finding is not universal, however. In Ghana, for example, it was demonstrated that the impact of insurance was very large for the poor.30 40 In Ghana, the poor are enrolled free of charge and do not incur any co-pay when using services. Therefore, the parameters are similar in theory to those in Senegal. One reason for the difference in impact on the poor, however, may be that in Ghana there are no financial barriers to access for the poor, whereas in Senegal some CBHI schemes create restrictions when beneficiaries of the PNBSF scheme seek access to services.60 Some community mutual health insurance companies refuse to finalise the registration of PNBSF members or do not agree to take them on, which explains the significant gap between expected members (21.53%) and actual members (2.36%). The mutual health insurance companies explain these practices by the delays in the payment of the subsidies to the contributions promised by the government.60

We also attempted to draw additional insights by conducting a detailed analysis of the effects of the schemes by type of service and level of provider (health post, health centre and hospital), looking jointly at the frequency of use and the level of out-of-pocket expenditure for each item. This joint analysis of the two dimensions of UHC is essential for an unbiased assessment of the impact of health insurance.43 Indeed, more frequent use of health services among the insured does not necessarily mean that insurance improves access to care. It may simply be that people who are sick more often have a greater tendency to be insured.44 This attitude, referred to as adverse selection, is common when health insurance is voluntary.61 Therefore, it is essential to observe the trend in out-of-pocket expenses as well. Similarly, restricting the analysis to the impact of out-of-pocket expenditure can be misleading. Low health expenditures may simply be the result of low utilisation of care, not of health insurance coverage. The implementation of this joint analysis shows that the PNBSF scheme has a significant impact for the non-poor at the highest level of the health pyramid, that is, in public hospitals. They are more likely to access and spend less in hospitals than the uninsured, which is not the case for the poor. The poor have a lower probability of accessing both hospitals and health centres (called ‘district hospitals’ in other countries), even though they face higher out-of-pocket expenditure than the uninsured. This difference between the poor and the non-poor within the same scheme may be puzzling, especially since, in principle, beneficiaries do not contribute and do not incur co-pays at the time of seeking care. However, these results may indicate the existence of additional costs linked to accessing hospitals, which are a deterrent for the poor, or other non-financial barriers. It is also possible that the poor live-in areas far away from hospitals (which tend to be in urban areas) and prefer going to the health post to avoid transport costs. A study in Burkina Faso, where the poor were well covered by CBHI, found that if they lived far away from health facilities, they were more likely to forego care.62

Limitations of the study

The first limitation of the study is that its results may not be transposable to the entire country because the data are only from 3 regions out of the 14 in Senegal, which were not selected for their representativeness, but rather because they correspond to the intervention zone of the donors who financed the survey.

In addition, we chose to treat as two distinct schemes, the partially contributory scheme, open to the entire population and the unremarkable scheme reserved for beneficiaries of the grant programme for poor families. However, these schemes are sometimes assimilated by the CBHI organisations, who are in charging of providing them, as a unique scheme. As a result, our separation of these schemes may not necessarily reflect the reality in some other localities.

Conclusion

Our study has shown that CBHI has an impact on the non-poor but do not sufficiently protect the poor. The major lesson we learnt, related to our main objective of assessing the impact of CBHI on the poor, is that it is important to specifically address the issue of insuring the poor. A programme designed for the general population is likely to be ineffective, or at least insufficiently efficient, for the poor. The question of access to free care for the latter, without any form of contribution, either to access insurance or as a co-pay, should be seriously considered in a context where more than a quarter of the population lives on less than US$3.2 per day. Furthermore, such a quantitative study would need to be complemented by a qualitative study to better understand the non-financial barriers to accessing care, which may disproportionately affect the poorest.

Data availability statement

Data are available on reasonable request. Data are available on reasonable request. The study data are not available in a repository, but sharing will be considered by request.

Ethics statements

Patient consent for publication

Ethics approval

The survey was approved by the National Health Research Ethics Committee. We carried out a secondary exploitation of the anonymised data. The approval reference is: Protocol SEN18/36. Participants gave informed consent to participate in the study before taking part.

References

Footnotes

Contributors MSL, AF and MFB conceptualised the study. MSL undertook the analyses and prepared the initial draft of the paper. AF validated the method and the different results. MFB refined the various versions of the full paper. MSL, AF and MFB approved the final manuscript for submission. The corresponding author attests that all listed authors meet authorship criteria and that no others meeting the criteria have been omitted. MSL are the guarantor for the data used for the analyses.

Funding The authors have not declared a specific grant for this research from any funding agency in the public, commercial or not-for-profit sectors.

Competing interests MSL is the legal director of the Senegalese agency in charge of the supervision and financing the CBHI. No conflicts declared for AF and MFB.

Patient and public involvement Patients and/or the public were not involved in the design, or conduct, or reporting, or dissemination plans of this research.

Provenance and peer review Not commissioned; externally peer reviewed.