Article Text

Abstract

Objective The purpose of this study is to assess the impact of microfinance health interventions (health insurance and health-awareness programmes) on health-related outcomes among female informal workers in Pakistan.

Design We conducted a retrospective, quasi-experimental study among a total of 442 female borrowers from seven microfinance providers (MFPs) across four provinces of Pakistan in 2018. A standardised tool was used for data collection. Probit regression was used to identify the probability of female borrowers gaining improvements in health outcomes based on their sociodemographic characteristics. Propensity score matching (PSM) was used to assess the overall impact of health interventions.

Primary outcome measures Four health-related outcomes reported by the women were used: perception of good health overall, ability to visit a general practitioner, ability to purchase prescribed medicine and intake of multivitamins.

Results We found that women receiving health interventions had a greater probability of better health outcomes when they were from Punjab province, borrowing in groups and attending monthly meetings at MFPs. Even with a small loan amount, all four health-related outcomes were significantly associated with receiving health insurance and health-awareness programmes. PSM results show a greater likelihood of overall perceived good health (nearest neighbour matching (NNM) =17.4%; kernel matching (KM) =11.8%) when health insurance is provided and a significant improvement in the ability to purchase prescribed medicine when a health-awareness programme is provided (NNM=10.1%; KM=11.7%).

Conclusion Health and social policies are vital to secure health and well-being among poor women working in the informal sector. Targeting improved equity across female population groups for health interventions will in the long run improve poor women’s health, income-earning abilities and capacity expansion for small businesses.

- health policy

- public health

- epidemiology

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

Strengths and limitations of this study

This study uses a nationally representative sample of 442 female borrowers of microfinance from four provinces in Pakistan.

It is the first study which focuses on female microfinance borrowers in Pakistan to assess the impact of health interventions on health-related outcomes among poor women.

We were able to identify health improvements when women received health insurance and health-awareness programmes.

Due to the cross-sectional study design and quasi-experimental analysis framework, the results must be interpreted with caution.

Future studies need to consider additional burdens of loan repayment and small-business investment.

Introduction

More than half (57%) of the female population of Pakistan is illiterate. Less than a quarter (23%) of women are employed, with a majority working in the informal sector.1 Informal workers in Pakistan are usually self-employed or involved in small-scale work. They are not protected by the country’s labour laws and regulations. Therefore, they do not receive employment benefits like a permanent contract, minimum wage, medical allowances, a pension or provident fund. There are several problems to consider with regard to the health of female informal workers in Pakistan, including high rates of poverty and low health literacy, as well as inadequate access to public health services,2 reinforced by low government health budget allocations for this population group.3 In addition to the overall absence of universal health coverage, there is limited coverage for public health emergencies like pandemics4 and greater risks of acquiring infectious diseases among female informal workers due to mostly unsanitary living conditions in disadvantaged communities.5 Pakistan has one of the largest out-of-pocket healthcare expenditures globally, at an overwhelming proportion of 90%.6 Although health insurance can become an important support system for buffering the poor against out-of-pocket payments, so far it covers only 1% of health expenditure in the country.2 This is because health insurance is mainly used by richer and urban populations.

The efficacy and limitations of private providers of health interventions in Pakistan are not clear. One of the few private providers offering health interventions to women employed in the informal sector are microfinance providers (MFPs)(including banks, institutes and non-governmental organisations (NGOs)).7 MFPs are mainly operational in underdeveloped communities, providing loans to the poorest women for small-business development.8 There are 50 MFPs operating in Pakistan, with nearly 40 reporting some form of health intervention for clients, including health insurance and health-awareness programmes.9 The MFPs are regulated either by the State Bank of Pakistan or the Securities Exchange Commission of Pakistan. An inherent function of the original model of microfinance was to catalyse wider social development for women, including improved health behaviour and, therefore, better health-related outcomes.10 It is in the interests of MFPs to couple health interventions with loan services because healthy clients are more likely to repay loans and run successful businesses.11

The role of microfinance health interventions is critical in countries like Pakistan, where poverty is high and out-of-pocket payments are not possible for impoverished families. Additionally, the public sector does not have a dependable service structure for complete or quality healthcare and universal financial protection for health coverage is absent.4 More than two million poor women are loan takers of microfinance in the country.12 As poor populations do not have the money to take out traditional health insurance, microfinancing for health insurance becomes the only option for them. However, small health insurance schemes have been severely criticised for their minimal impact on clients’ lives due to their minimal coverage and the large burden of disease faced by poor populations.13 Evidence also suggests that poor populations holding minimal health insurance, in the event of sustaining large healthcare costs, may resort to damaging practices such as reducing household nutrition, removing children from school and taking out more loans.14 During the most recent times of the coronavirus pandemic, debt-ridden poor women attempting to repay loans are facing even more challenges in generating income from small businesses due to social isolation and lockdown.15 Therefore, health security is a major concern among female borrowers and there is a need to improve research and policy in order to financially protect poor women and improve their health literacy.16

Aims of the study

To the best of our knowledge, there are no studies that have used female microfinance borrowers as a sample to assess the impact of health interventions on health-related outcomes among poor women.17 Our objective for this study was to use a sample of female microfinance borrowers, who are availing themselves of health insurance from a private provider, to help identify suitable policies for disease prevention and health promotion in Pakistan. The following research questions are addressed in this study: (1) Do female borrowers of microfinance who are provided with health interventions show improved health-related outcomes? and (2) What are the sociodemographic, household and loan portfolio characteristics of female borrowers of microfinance that are associated with improved health-related outcomes?

Methods

This study is part of a larger, mixed-methods study on the well-being of female microfinance borrowers. The qualitative part has already been published.18 The results presented here are based on a cross-sectional survey, in which women who had been borrowers of microfinance for more than 1 year were interviewed using a structured, quantitative questionnaire. We used the framework of a quasi-experimental study to estimate the impact of microfinance health interventions. The data was analysed using SPSS version 25 and STATA 16.

Sampling

We used a list available on the Pakistan Microfinance Network to contact the 20 MFPs across Pakistan. Seven MFPs agreed to provide permission to interview their clients. The sampling took place in all four provinces of Pakistan (Punjab, Sindh, Balochistan, and Khyber Pakhtunkhwa (KPK)), but not in the two autonomous territories or the federal territory of Islamabad. The sampling frame at the level of individual women took the population weightage of the provinces into account. We were able to contact 500 women randomly, as they visited the MFP offices to make their monthly loan repayment. A final total of 442 women were willing to participate and provided informed written consent, which is a response rate of 88.4%. These women were sampled from seven cities within the four provinces, based on MFP permission and access (Punjab: n=252 (cities: Gujranwala, Lahore, Khanewal, Sheikhapura); Sindh: n=100 (city: Matiari); Balochistan: n=50 (city: Lasbela); KPK: n=40 (city: Abbottabad)). Study participants received financial support from the following types of MFPs: four microfinance banks (n=340), one microfinance institute (n=41), one government microfinance scheme (n=50) and one Islamic microfinance organisation (n=11).

Information related to the services provided by the sampled MFPs in this study is presented in table 1. None of the MFPs provide mandatory health insurance schemes. Neither the government scheme nor the Islamic finance provider were offering health insurance, but they were providing health-awareness interventions. The government scheme offered a separate health insurance scheme (called the Sehat Sahulat Programme), but none of the study participants was enrolled in this scheme. Women borrowing from banks have the option to take out health insurance for themselves and any family members. They have to pay a premium ranging from PKR490–PKR990 (US$3.00–US$6.08) (all PKR to USD conversions in this study have been done at the rate of 1 USD=162.805 PKR.) per person and are insured only in the event of hospital admission. However, the insurance does not cover hospital costs but instead pays the client the amount of daily wages lost, ranging from PKR2000–PKR4000 (US$12.28–US$24.56) daily. The scheme also covers a one-off payment in the event of death, ranging from PKR25 000–PKR50 000 (US$153.55–US$307.10). Female borrowers from the microfinance institute are only covered for themselves and their spouse. They have to pay a premium of PKR1200 (US$7.37) if unmarried or PKR1850 (US$11.36) if married. Clients are provided with a one-off payment of PKR30 000 (US$184.25) in the event of hospitalisation.

Health insurance schemes of microfinance providers (MFPs) sampled in this study

Data collection

Data collection took place between February and November 2018. Each city had one research team leader and two assistants in the data collection team, comprising a total of 21 people undertaking data collection. The assistants were all MPhil graduates who had experience of field research and were hired through the assistance of the universities in each city. Training of the data collection team took place over a 2-week period and was conducted either in person or through video calls. Data collection took place in face-to-face interviews in a private space at the MFP premises, in order to preserve the women’s privacy due to the personal nature of the questions. The structured surveys were completed on behalf of the female respondents with the assistance of the trained research team. During pilot testing, we used both a self-administered and researcher-administered approach, and found that the latter showed lower rates of non-response. This could be due to the length of the questionnaire and the low literacy rate among the interviewed women. Although the questionnaire was translated into Urdu, women having less than 8 years of schooling required assistance to read and fill in the questionnaire.

Measures

A structured interview schedule was used for data collection (online supplemental file 1). Questions in this tool were taken from instruments used in various studies, such as the Women’s Healthcare Experiences Survey,19 the Baseline Nutrition and Food Security Survey developed by UNICEF,20 the WHO Multi-Country Study on Women’s Health and Domestic Violence against Women,21 and the WHO Survey on Workplace Violence.22

Supplemental material

Dependent variables: health outcomes

This study assesses the association of health interventions offered by MFPs with four dependent health-related outcome variables: (1) women perceive health to be good overall, (2) women visited a general practitioner in the last year, (3) women had the ability to purchase prescribed medicine in the last year and (4) women’s intake of multivitamins has improved in the last year. The four dependent variables were categorised as binominal and coded as either ‘yes’ (1) or ‘no’ (0).

Independent variables: sociodemographic and loan characteristics

Several sociodemographic variables, such as age (0=less than 30 years; 1=30 years and older), religion (0=Muslim; 1=other than Muslim), literacy of the female borrower (0=illiterate; 1=literate), literacy of the spouse (0=illiterate; 1=literate), house ownership (0=yes; 1=no) and number of dependent children living in the house (0=none; 1=one or more) were assessed as confounding variables. It is necessary to control for these variables because they have an impact on each of the dependent variables mentioned above. Province is also controlled because the region is a proxy for sociocultural norms that would impact on how women perceive their health and whether they are able to visit a general practitioner or purchase medicine (0=other than Punjab [(Sindh, Balochistan or KPK); 1=Punjab).

The other set of variables is related to MFP services, such as: loan amount (0=PKR10 000–20 000; 1=PKR21 000 or more), monthly meetings (0=no; 1=yes), interest rate, which is the amount charged on top of the principal by a lender to a borrower (0=2.5%–10%; 1=11% or more), group loan, meaning that a group of customers are willing to guarantee each other for the repayment of the loan (0=no; 1=yes), and debt age (0=1–2 years; 1=3 or more years). These have been included because they assess the impact of the provision of non-financial services on each of the dependent variables.

Independent variables: health intervention

The three independent variables for microfinance health intervention are: (1) receiving health insurance, (2) attended at least one health workshop and (3) received health-related talks by loan officers. The two independent variables of health workshop and health-related talks by loan officers were compounded to make one variable indicating whether the women had attended a health-awareness programme (0=no; 1=yes). In this way, the control group for the study (T=0) consists of female borrowers who lack the provision of a health intervention, and the treatment group (T=1) includes female borrowers who are receiving a health intervention.

Comparison group

Using a quasi-experimental framework, the study estimates the impact of gaining access to health interventions (health insurance and health-awareness programmes) against the counterfactual of those women who are receiving a loan for small business mobilisation in the absence of health interventions.

Probit analysis

The impacts of health insurance and health-awareness programmes provided by the MFP on the four dependent, health-related variables have first been estimated using a probit estimation for the following linear regression equation:

where  is the dependent variable measuring the four health-related outcomes. T is the treatment variable (1 if ‘yes’, and 0 otherwise) measuring the three microfinance health interventions.

is the dependent variable measuring the four health-related outcomes. T is the treatment variable (1 if ‘yes’, and 0 otherwise) measuring the three microfinance health interventions.  is a set of sociodemographic characteristics including age, religion, province and literacy;

is a set of sociodemographic characteristics including age, religion, province and literacy;  is a set of household characteristics, including house ownership and number of dependent children living in the house;

is a set of household characteristics, including house ownership and number of dependent children living in the house;  is a set of loan portfolio characteristics including debt age, group loan, loan amount, interest rate and monthly meetings; and

is a set of loan portfolio characteristics including debt age, group loan, loan amount, interest rate and monthly meetings; and  is the error term.

is the error term.

Propensity score matching

We used propensity score matching (PSM) to estimate the unobserved counterfactuals and make an impact analysis of health interventions. PSM is a non-parametric statistical method which matches the treated (those receiving the health intervention) and the controlled on the basis of conditional probability of participation, given the observable characteristics.23 As we only have cross-sectional data, we can compare the dependent variables related to women’s health in terms of those who have access to non-financial, health-related services provided by the MFP (in this study called the ‘health-awareness programme’) and those who do not, as long as these services are randomly distributed and there is no selection bias. The estimation of instrumental variables is one technique that is frequently used within PSM. However, these results are only robust if a valid instrument is being used. As it was not easy to find a valid instrument for our study, we used statistical matching, which has also been widely used before.24–26

The study will be using the following functional form:

where  is the dependent variable measuring the four health-related outcomes. T is the treatment variable (1 if ‘yes’, and 0 otherwise) measuring the microfinance health interventions.

is the dependent variable measuring the four health-related outcomes. T is the treatment variable (1 if ‘yes’, and 0 otherwise) measuring the microfinance health interventions.  are the covariates used for matching the data, including age, religion, literacy, spouse’s literacy, house ownership, access to drinking water, access to gutter drainage, access to toilet facility, children, debt age, group loan, loan amount, interest rate and monthly meetings, and

are the covariates used for matching the data, including age, religion, literacy, spouse’s literacy, house ownership, access to drinking water, access to gutter drainage, access to toilet facility, children, debt age, group loan, loan amount, interest rate and monthly meetings, and  is the error term. These control variables have been used in a large and growing volume of studies.27

is the error term. These control variables have been used in a large and growing volume of studies.27

Our study satisfies the main conditions of PSM, which are: (1) using a rich set of control variables, which are observable characteristics, (2) using the same survey for treated and control groups and (3) having the same community belonging to the treated and control groups.28 The PSM model constructs a statistical comparison group based on the probability of participating in the treatment T, conditional on observed characteristics, X, or the propensity score:

where T = {0, 1} is the indicator of exposure to treatment and X is the multidimensional vector of pretreatment characteristics. Following the estimation of the propensity score, the region for common support is defined as being where distributions of the propensity score for the treatment and comparison group overlap. Observations within the control and treatment group that lie outside the region for common support are eliminated.29 As PSM is intended to help in identifying the impact of the health intervention, we used the computation of ‘average treatment effect on the treated’ . We used two matching criteria (nearest neighbour matching (NNM) and kernel matching (KM)), to assess statistical significance from different perspectives and to test the robustness of the results.24 NNM is used to evaluate absolute differences between propensity scores, and KM is used to compare each treated unit to a weighted average of the outcomes of all untreated units.

Patient and public involvement

This research was conducted without the involvement of the public or patients. However, the views of women from this study have been published elsewhere.18

Results

Sample characteristics

All the women in our sample earned less than US$4.82 per day and belonged to the poorest stratum of society. They were taking out loans for small business mobilisation in order to improve their life opportunities. The majority of the women were Muslim, from Punjab and illiterate. About three-quarters had been borrowers for more than 3 years, were attending monthly meetings with loan officers, and were paying interest rates of less than 10%. Out of the 442 female borrowers in the sample, 64.2% (n=284) had taken out health insurance (table 2) and 71.0% (n=314) had participated in a health-awareness programme by attending a health workshop or receiving health talks by loan officers (table 3).

Descriptive statistics of women borrowers with regard to health insurance

Descriptive statistics of women borrowers with regard to health awareness

Determinants of health-related outcomes after the health insurance intervention

Table 4 presents the determinants of health-related outcomes for recipients of health insurance. Overall, perceived good health was significantly associated with group borrowers, small loan amounts and lower interest rates. Improved ability to visit a general practitioner shows a positive correlation with female borrowers from Punjab province, who attending monthly meetings, had a group loan and a smaller loan amount. Women had a significantly improved ability to purchase prescribed medicine when they were from Punjab, took out smaller loans and owned a house. The uptake of multivitamins was increased among women with smaller loans, who owned a house, had been borrowers for no longer than 2 years, and were attending monthly meetings. Therefore, only a small loan amount was a significant determinant in all four health-related outcomes among recipients of health insurance.

Probit analysis on determinants of health-related outcomes among recipients of health insurance

Determinants of health-related outcomes after the health-awareness intervention

In table 5, the determinants for all four health-related outcomes among recipients of a health-awareness programme are presented. Women with the following characteristics have a greater probability of overall perceived good health: group borrowers, smaller loans, lower interest rates, younger women and those with literate spouses. The ability to visit a general practitioner for regular check-ups during the previous year was higher among women from Punjab province, with smaller loans, attending monthly meetings, above 29 years of age and who were non-Muslim. Similarly, women from Punjab province, having smaller loans, owning their house and younger women had a higher probability of improved ability to purchase prescribed medicine. The probability of increased uptake of multivitamins was greater in women who took out smaller loans, had not been in debt for more than 2 years, were group borrowers and who attended monthly meetings. The only variable that was significantly associated with all four health-related outcomes among recipients of a health-awareness programme was the small loan amount.

Probit analysis on determinants of health-related outcomes among recipients of health-awareness programmes

Balancing covariates and common support diagnostics

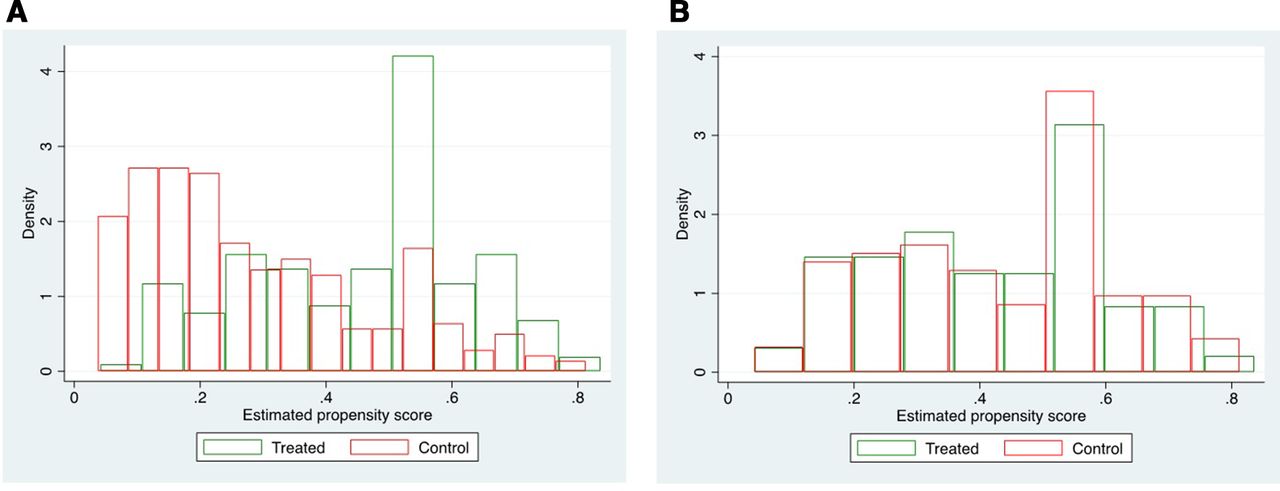

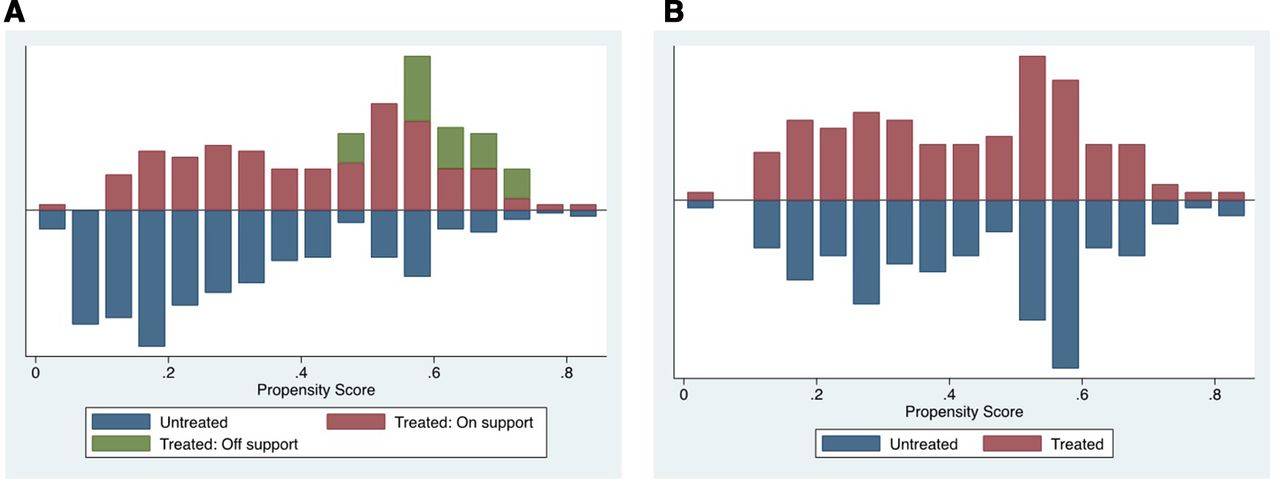

(a) Figure 1A exhibits the kernel density graphs for the propensity score of treated and control groups before matching, while figure 1B exhibits it after matching. It can be clearly seen that the kernel densities are significantly overlapping in the latter, indicating that the treatment and control groups have a comparable propensity score as estimated using the covariates. A similar comparison of treatment and control groups can be observed in figure 2A and B using histograms.

Kernel density plot (A) before and (B) after matching.

Density balancing plot (A) before and (B) after matching.

Figure 3A and B exhibits the common support between the control and treatment groups. While in figure 3A, we can see that certain observations in the treated group are not matched, in figure 3B all the observations in the treated and control groups are successfully matched.

{kind=link}

{kind=link}

{kind=link}

Common support graph of propensity scores (A) before and (B) after matching.

The balancing of covariates can also be observed using standardised mean difference and ratio of variances. Table 6 gives the standardised mean difference and ratio of variances for the control and treatment groups before and after matching. It can be observed that the standardised mean difference in the matched sample is much improved and close to zero for all covariates. The ratio of variances is approximately equal to one in the matched sample for all covariates except monthly meetings. Using these diagnostics, we can infer that the sample has matched well using PSM.

Balancing of covariates using standardised mean difference and ratio of variances

Impact of the interventions on health-related outcomes

The descriptive statistics for comparison between control and treatment group for health insurance (online supplemental table 1) and the health-awareness programme (online supplemental table 2), before and after matching, depict the elimination of imbalance with respect to almost all covariates before and after matching. Table 7 shows that women receiving health insurance had a significantly greater chance of overall perceived good health. According to NNM, 17.4% of women with health insurance had a greater likelihood of overall perceived good health; the results for KM showed a greater likelihood in 11.8%. Female borrowers receiving a health-awareness programme from the MFP in the form of a health workshop or health talk by the loan officer show a significant improvement in their ability to purchase prescribed medicine (NNM=10.1%; KM=11.7%). For the other two outcomes, neither of the interventions showed a significant effect.

Supplemental material

Impact of interventions on health-related outcomes based on propensity score matching

Discussion

In the absence of universal health coverage or compulsory educational enrolment, poor and predominantly illiterate female informal workers and borrowers of microfinance are dependent on MFP for receiving health coverage and promoting health. This study has measured four health-related outcomes in female borrowers. The results show that there is inequity in the uptake of health insurance and health-related outcomes.

Women from Punjab have better health-related outcomes compared with women from Sindh, Balochistan and KPK. National health surveys of Pakistan also report that Punjab has better health-related outcomes compared with other provinces, because the provincial government of Punjab has a greater budget allocation for running health-awareness campaigns.30 The fact that our results show that older women and non-Muslim women have a greater likelihood of improved ability to visit a general practitioner after receiving a health-awareness intervention indicates that younger Muslim women face barriers to healthcare access due to regressive norms.31 Muslim families are known to prevent fertile women from accessing healthcare in an attempt to control their reproductive choices and health options. Our results align with other research, which suggests that Muslims suffer from health disparities due to religious fallacies.32

Conversely, younger women show better overall perceived health and ability to purchase prescribed medicine. This may be because at a younger age fewer health issues occur, and also because of greater state and NGO efforts directed towards maternal healthcare.33 Our results confirm that women under the age of 29 years receive privileged support in a patriarchal society during their prime childbearing years to consume maternal health-related medication.34 Women with literate spouses also show improvements in overall general health after receiving health insurance. This may be because spouse literacy has a direct effect on women’s improved healthcare behaviour and mental health.35

Women who take out their loan in groups show better health-related outcomes compared with women who are single borrowers. Our results suggest that women in groups share their healthcare knowledge and encourage each other towards improved healthcare behaviour.36 Similarly, women who attend monthly meetings with loan officers have better health-related outcomes. The results suggest that caring loan officers are fulfilling an important responsibility in supporting female borrowers to engage in improved health behaviour and health-related outcomes. Given the conservative culture of Pakistan and the disadvantaged backgrounds of these female borrowers, loan-taking women might not be able to use healthcare services due to issues of permission or ignorance.

Women who receive smaller microfinance loans and do not have a long debt age show improved health-related outcomes. The finding that only women who receive smaller loans show significantly better health-related outcomes may be seen as an endogenous result (ie, because individuals who need only a small loan may be better off to start with in terms of health), and difficult to interpret in terms of causality, given the cross-sectional nature of the data. However, we have only sampled women from the poorest stratum, and they have taken out small loans because they are not eligible for bigger loans. Therefore, one can expect that there is no association between health condition at the time of loan taking and the loan amount.

Furthermore, the finding related to debt age suggests that women with a debt burden over a longer period of time may be suffering from debt fatigue, which is converting to declining health-related outcomes.37 Women and their families who own their houses also have better health-related outcomes, specifically related to the ability to visit general practitioners and improved uptake of multivitamins. The results imply that the provision of health insurance and not having to pay household rents on a monthly basis translates into better health-related outcomes. Impoverished families who have to pay high rents for accommodation are usually employed in multiple jobs and have little time for health and well-being.38

The impact of microfinance is only visible on two health-related variables. Although there are no effects on general practitioner visits or uptake of multivitamins, we found that microfinance health insurance has an impact by creating an improved perception of general health. This shows that being insured is an emotional support and well-being facilitator for poor women. The emotional buttress provided by health insurance can go a long way towards improving perceived well-being, which can translate into a greater commitment to self, family and business development among poor women from disadvantaged backgrounds.39 In addition, microfinance health-awareness interventions have an impact by improving the purchase of prescribed medicine. Many poor women in Pakistan do not take prescribed medicine unless it is freely available due to the greater need to prioritise the purchase of basic necessities and household consumption.40 The impact of microfinance interventions is comparable to previous research. A review highlighted that most interventions combined microfinance with health education. However, positive effects were mainly found for health knowledge and behaviour, but not health status.41 A meta-analysis indicated the potential for women and girls, because microfinance may lead to changes in the use of contraceptives, strengthen female empowerment and improve children’s nutrition.42

However, for female borrowers of microfinance, there might be additional burdens in the form of loan repayments and small-business investment. Our results suggest that illiterate and poor women in the country are benefiting from health awareness by recognising that if they do not consume prescribed medicine for chronic ailments (heart disease, cholesterol or diabetes) it can have serious consequences for their own lives and the future livelihood of their families. There needs to be an urgent recognition that a triadic health insurance safety net is necessary, instead of dependency on private providers to protect informal working women in Pakistan. Employers and the government must join forces to ensure universal health insurance and—particularly in these times of the coronavirus pandemic—infectious disease outbreak insurance for health emergencies. State financing of healthcare is essential through an increased allocation of gross domestic product (GDP), government-run business profits, and increasing the income and corporate tax base from the elite.

With regard to female microfinance borrowers, we recommend microfinance regulatory bodies to urgently legislate the following reforms: (1) coverage for children and other dependents, maternity costs, and non-hospitalisation costs, (2) expand coverage for religious and ethnic minorities, (3) reduce interest rates for those paying high housing rents and introduce home ownership loans, (4) introduce mandatory group borrowing and monthly meetings with loan officers and (5) alter repayment timelines and interest-rate packages for women taking out bigger loans.

We recommend the following urgent social policy improvements, which would join in helping health policy efforts: (1) the development of public primary healthcare services for women in the communities, with a mandatory quarterly general practitioner meeting, 2) the upgrading of poverty alleviation programmes to support poor women, (3) the capping of housing rents and improvements in neighbourhood sanitation to curb infection, (4) the advancement of home-based business opportunities for informal female workers to assist in maintaining incomes, including digitalisation and internet access in their homes and (5) income supplementation and cash transfers for multivitamins and food nutritional intake to improve overall immunity and health.43

Limitations

This study has some limitations, most importantly the cross-sectional design. Although we were able to compare the effects of an intervention because of the quasi-experimental analysis framework, two-group cross-sectional designs suffer from the limitations related to a single measurement for all subjects. Therefore, within-person changes over time are not observable. Without repeated measures in a two-group design, causality cannot be identified, because temporal sequencing on the intervention and outcomes cannot be established. For that reason, we recommend longitudinal data collection in future studies. This study focused on comparatively small loans. Therefore, the impact of larger loans (>PKR100 000) on health is not known. Furthermore, the results need to be interpreted with caution, because the four health-related outcomes are non-homogeneous and dependent on socioenvironmental factors that are specific to the region and community where the interventions are taking place. In addition, outcome data are based on self-reporting, which can lead to potential measurement errors. Despite these limitations, we feel that this study is significant for the development of microfinance health services in Pakistan and the role of state and interest-free microfinance health interventions.

Conclusion

It is critical to assess the health needs of women employed in the informal sector. As primary caregivers at home as well as primary contributors to household income, women’s health assumes a salience that could place the structures of both the family and the economy at risk. Health policy must consider several social policies for protecting disadvantaged women, who are poverty ridden, illiterate or semiliterate and loan takers. Health insurance schemes and health promotion in the workplace must be made mandatory for employers, MFPs and the government, given the cultural barriers to uptake for women. Targeting improved equity across female population groups for health interventions will in the long run improve women’s health, capacity expansion and income-earning abilities.

Designing and implementing a health and social policy protection net for female informal workers requires empirical evidence regarding which health interventions and sociodemographic characteristics impact on health outcomes. Since public-sector and health-sector shortages and inefficiencies are a concern in Pakistan, the ‘health card’ must be accepted in both the private and public sector, whichever is able to serve the poor first. As Pakistan is struggling with a low GDP and tax collection base, we recommend more research into options for social franchising, and partnerships with independent health insurance companies to serve disadvantaged women.

Acknowledgments

We thank the female borrowers who consented and gave their time to participate in the study. We are grateful to our research team members in charge of logistical planning and coordination for data collection across Pakistan including Rizwan Haider and Amir Naseem. Individual data collection heads for each city are thanked for their efforts, especially for resolving gate keeping issues, including Nida Abbas (Lahore), Zainab Asif (Abbotabad), Hina Bukhari (Gujranwala), Sadia BiBi (Khanewal), Ansari Abbass (Sheikhapura), Azra Shakeel and Shumaila Sadique (Matari), and Javaria Imran (Lasbela). The research assistant Bilal Asghar is also thanked for entering all data.

We acknowledge support from the German Research Foundation (DFG) and the Open Access Publication Fund of Charité – Universitätsmedizin Berlin.

References

Supplementary materials

Supplementary Data

This web only file has been produced by the BMJ Publishing Group from an electronic file supplied by the author(s) and has not been edited for content.

Footnotes

Twitter @JafreeRizvi

Contributors SRJ designed the study and was responsible for the research project, including data collection and analysis; FF supervised this process. HA and MM supported in data collection. RZ and FF contributed to the interpretation of the data. SRJ drafted the manuscript; all authors revised it critically for important intellectual content. All authors approved the final version of this manuscript.

Funding This study received funding by the Office of Research, Innovation and Commercialisation at Forman Christian College. The grant number is IRB-180/04-2017.

Disclaimer The funding body was not involved in data collection, data analysis, or data interpretation and presentation.

Competing interests None declared.

Patient consent for publication Not required.

Ethics approval Ethical approval for this study was taken from the Institutional Review Board of the Forman Christian College.

Provenance and peer review Not commissioned; externally peer reviewed.

Data availability statement Data are available from corresponding author on reasonable request.

Supplemental material This content has been supplied by the author(s). It has not been vetted by BMJ Publishing Group Limited (BMJ) and may not have been peer-reviewed. Any opinions or recommendations discussed are solely those of the author(s) and are not endorsed by BMJ. BMJ disclaims all liability and responsibility arising from any reliance placed on the content. Where the content includes any translated material, BMJ does not warrant the accuracy and reliability of the translations (including but not limited to local regulations, clinical guidelines, terminology, drug names and drug dosages), and is not responsible for any error and/or omissions arising from translation and adaptation or otherwise.