Article Text

Abstract

Objectives The study aimed to understand the impact of integrating a fee waiver for the National Health Insurance Scheme (NHIS) with Ghana’s Livelihood Empowerment Against Poverty (LEAP) 1000 cash transfer programme on health insurance enrolment.

Setting The study was conducted in five districts implementing Ghana’s LEAP 1000 programme in Northern and Upper East Regions.

Participants Women, from LEAP households, who were pregnant or had a child under 1 year and who participated in baseline and 24-month surveys (2497) participated in the study.

Intervention LEAP provides bimonthly cash payments combined with a premium waiver for enrolment in NHIS to extremely poor households with orphans and vulnerable children, elderly with no productive capacity and persons with severe disability. LEAP 1000, the focus of the current evaluation, expanded eligibility in 2015 to those households with a pregnant woman or child under the age of 12 months. Over the course of the study, households received 13 payments.

Primary and secondary outcome measures Primary outcomes included current and ever enrolment in NHIS. Secondary outcomes include reasons for not enrolling in NHIS. We conducted a mixed-methods impact evaluation using a quasi-experimental design and estimated intent-to-treat impacts on health insurance enrolment among children and adults. Longitudinal qualitative interviews were conducted with an embedded cohort of 20 women and analysed using systematic thematic coding.

Results Current enrolment increased among the treatment group from 37.4% to 46.6% (n=5523) and decreased among the comparison group from 37.3% to 33.3% (n=4804), resulting in programme impacts of 14 (95% CI 7.8 to 20.5) to 15 (95% CI 10.6 to 18.5) percentage points for current NHIS enrolment. Common reasons for not enrolling were fees and travel.

Conclusion While impacts on NHIS enrolment were significant, gaps remain to maximise the potential of integrated programming. NHIS and LEAP could be better streamlined to ensure poor households fully benefit from both services, in a further step towards integrated social protection.

Trial registration number RIDIE-STUDY-ID-55942496d53af.

- health policy

- public health

- economics

- cash transfers

- health insurance waivers

- Ghana

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

Strengths and limitations of this study

This is the first study to assess the impact of an integrated government programme providing cash transfers combined with a fee waiver for a national health insurance scheme on health insurance uptake.

We use a quasi-experimental, longitudinal, mixed-method study design to examine causal impacts of the intervention on health insurance enrolment.

This study demonstrates that while integration of cash transfers with a fee waiver for health insurance can increase the enrolment, large gaps remain.

A limitation of the study design is that it estimates local average treatment effects, and thus programme effects may be larger for individuals in poorer households, further from the proxy means test cut-off used in our sampling criteria, compared with impacts estimated in this study.

Introduction

Poverty is a determinant of poor health and reduced access to healthcare, compounding the former. Increasingly, social protection programmes are being implemented globally to reduce poverty and promote increased investment in human capital development, including health.1 A common social protection programme is cash transfers, which entail direct provision to cash to beneficiary households. Robust evidence demonstrates impacts of cash transfer programme on poverty reduction, food security and increased healthcare expenditure and utilisation.2–5 Existing literature related to health outcomes and health seeking comes largely from Latin America, where cash transfer programmes tend to be conditional on health check-ups and other ‘co-responsibilities’, whereas African programmes are largely unconditional, meaning there are no behavioural requirements to maintaining eligibility.

Moreover, impacts of these programmes on health outcomes and behaviours have been less studied in Africa, particularly in the context of unconditional government cash transfer programmes (which make up the majority of government cash transfers in Africa), such as Ghana’s Livelihood Empowerment Against Poverty (LEAP) programme. One notable exception to the regional gap in evidence is a study that examined evidence from a conditional (on school attendance and health clinic visits) cash transfer programme in Tanzania that informally encouraged enrolment in community-based health insurance. The study found that the programme increased health insurance take-up and likelihood of seeking care when ill, however, increases in health seeking, as measured by clinic visits, took time to materialise (1.5 years) and disappeared after 2.5 years. Impacts of cash transfer programmes on health-related outcomes may vary based on context and programme design, including transfer amount and frequency, targeting, and conditions or ‘co-responsibilities’. Thus, more research is needed on the topic, especially from unconditional programmes.

In Ghana, socioeconomic gaps in health outcomes and access to healthcare persist. For example, populations in the lowest wealth quintiles are more likely than those in the richest quintile to experience teenage pregnancy, under-5 mortality, child mortality, have no vaccinations, and experience stunting, and are less likely to use modern contraceptives or deliver at a health facility.6 7

To mitigate the impact of poverty on health, integrated programming and linkages to services are needed. Linking cash transfers with health insurance is an example of integrated social protection programming (sometimes referred to as ‘cash plus’).8 While enrolment in health insurance does not guarantee access to health or improved health outcomes, it is an important first step to mitigating financial barriers and avoiding catastrophic expenditures. One study from Ghana showed that subsidies effectively promoted enrolment into National Health Insurance Scheme (NHIS)9; however, the question of whether a large-scale government-run cash transfer programme linked with fee waivers can induce beneficiaries to enrol in health insurance has not been examined.

In the past 15 years, the Government of Ghana has implemented two major policy initiatives to address the intersection of poverty and health. In 2003, government passed the National Health Insurance Act (Act 650) and established a National Health Insurance Authority (NHIA). Implementation of the NHIS began in 2004. The NHIS aims to remove cost barriers to accessing care and covers outpatient and inpatient services, dental services and maternal health services. The NHIA actively seeks out opportunities to enrol poor and vulnerable persons onto the scheme, as illustrated by their programme goals and targeted outreach to enrol members under the ‘indigent’ exemption.10 Act 650 exempted the following groups from paying the NHIS premium: persons classified as poor or indigent, persons over 70 years, children under 18 years, contributors to the Social Security and National Insurance Trust (SSNIT) and pensioners of the SSNIT. Then in 2012, the National Health Insurance Act (Act 852) replaced Act 650 (2003) and expanded these waiver-eligible categories to include persons in need of antenatal, delivery and postnatal healthcare services; persons with mental disorder; and persons categorised as disabled and determined to need social welfare support. It is estimated that over 60% of current NHIS enrollees are exempted from paying premiums,10 11 which make up a small proportion of total funding of the NHIA (estimated at 3% of total revenue).12 The largest sources of revenue for the NHIA are the National Health Insurance Levy (NHIL; a 2.5% levy on goods and services collected under the Value Added Tax) and SSNIT contributions (72% and 20%, respectively).12 Act 650 originally stipulated that individual premium amounts were set at the district level by district mutual health insurance schemes (DMHIS) and approved by the NHIA, ranging from approximately 7.2 to 48 Ghana Cedis (GH₵). However, in 2011, there was a review that adjusted the lower bound to 22 GH₵ while maintaining the upper bound at 48 GH₵. Act 852 (2012) then centralised the management of the scheme including the determination of premiums, and DMHIS no longer have the authority to determine premiums. Enrollees can obtain care from a variety of healthcare providers who are accredited by the NHIA, including public, faith-based, quasi-governmental and some private health facilities, pharmacies and chemist shops.13 This approach, whereby a purchasing agency (in Ghana, the NHIA) buys care from both public and private facilities, but maintains a parallel supply-side budget allocations from the government to public providers can also be seen in other middle-income countries implementing health insurance reforms with the aim of reaching universal health coverage.14

Annual renewal is required, given that individuals’ circumstances (eg, pregnancy, disability) may change, necessitating that they be placed into a different category, including those covered under premium exemptions. Annual renewal can be a barrier to maintaining enrolment, as a recent cross-sectional study of NHIS enrollees in one district in Ghana showed that dropout among enrollees is prevalent. It was estimated that 41% and 53% of enrollees in 2014 and 2015, respectively, dropped out the following year, and that those in the ‘indigent’ premium exemption category were significantly more likely to drop out.15

By 2014, NHIS coverage was estimated at approximately 40% of the population.16 Despite considerable progress in uptake, significant gaps remain, including limited knowledge of the scheme’s services and conditions, long waiting times, drug shortages and inadequate staffing of health workers, limiting access among the poorest and most marginalised populations.13 16 Among non-members of the NHIS, affordability of the premium and registration fees is commonly reported as a major barrier to enrolment.13 17 18 Indeed, a recent study examining ability to pay among household which opted not take up NHIS found that, while 66% of uninsured households were estimated to have the ability to afford the premiums, one-third were deemed unable to afford the premium.17

In a second major initiative to address extreme poverty, the Ministry of Gender, Children and Social Protection (MoGCSP) launched a large-scale social protection programme, the Livelihoods Empowerment Against Poverty (LEAP) in 2008. LEAP provides bimonthly cash payments ranging from 64 to 106 GH₵ to extremely poor households with orphans and vulnerable children, elderly with no productive capacity, persons with severe disability, and, starting in 2015, those with a pregnant woman or child under the age of 12 months. As of December 2017, LEAP reached more than 213 000 extremely poor families in all 216 districts of Ghana. In a step towards better integration of social protection programming, the NHIA and the MoGCSP collaborated in 2011 to enrol LEAP beneficiaries into NHIS, qualifying under the NHIA ‘indigent’ exemption which waives all NHIS fees, including those for card processing, premiums and renewals.

In the current paper, we assessed the impact of the integration of cash and fee waivers in LEAP 1000 on enrolment in the NHIS, hypothesising that the income effect of the cash transfers paired with the fee waiver would increase take-up.

Methods

Study setting and design

Data come from the impact evaluation of the Ghana LEAP 1000 pilot programme.19 This pilot added a fourth eligibility category to Ghana’s LEAP programme, namely, that of poor families with pregnant women (one eligible woman per household) or infants under 1 year old, aiming to reach poor children in the first 1000 days of their lives to improve nutrition and development (infants under 15 months were accepted as eligible to avoid excluding children due to variations in quality of birth date data and/or the extended duration of the targeting process). Now integrated into the LEAP programme nationally, LEAP 1000 was first piloted in 10 districts in northern Ghana. Programme participants are informed about the NHIS fee waiver eligibility at the time of enrolment, and awareness campaigns are periodically rolled out (including one during the study period). The longitudinal, mixed-methods evaluation was carried out by UNICEF Office of Research – Innocenti, the University of North Carolina at Chapel Hill (UNC-CH), the Institute of Statistical, Social and Economic Research (ISSER) of the University of Ghana, and Navrongo Health Research Centre (NHRC) and covered 5 of the original 10 LEAP 1000 pilot districts (Yendi, Karaga, East Mamprusi in the Northern Region and Bongo and Garu Tempane in the Upper East Region). These districts were purposively selected to reflect demographic diversity in the pilot. To identify a comparison group, the evaluation exploited the programme eligibility score (proxy means test, PMT) used in the targeting phase (March to July 2015) to identify eligible participants and collected data only on those households close to the cut-off for maximum comparability. This allowed for a regression discontinuity design (RDD) which focuses on observations near the cut-off, also referred to as local randomisation.20 We examined the satisfaction of RDD-related assumptions: first, the threshold for programme eligibility was determined by the government after PMT data were collected and based on the budget available, ensuring exogeneity of the cut-off point. Second, the distribution of the score around the cut-off did not show any discontinuity, indicating lack of manipulation of scores by participants to qualify for the programme. Third, the distribution of household characteristics and outcomes relative to the score at baseline had no discontinuity at the cut-off point and were statistically balanced. More details on the study design and baseline balance of household characteristics between study arms can be found in the baseline evaluation report (the success in the implementation of an RDD necessitates that (1) participants were not able to manipulate their PMT score, (2) the threshold is determined independently of the rating variable and (3) no discontinuities are present other than the treatment status in baseline characteristics and outcomes).21

The PMT includes assets, dwelling characteristics, household size and so on. Households falling below the cut-off, those classified as extremely poor by the PMT, were enrolled in the programme. The study was powered to detect programme impacts on child health and nutrition outcomes, with an estimated required sample size of 2500 households, half from the comparison group (above the PMT cut-off) and half from the treatment group (below the PMT cut-off). The baseline survey was conducted in July–September 2015 with 2497 women that were pregnant at the time of the targeting exercise or had a child under 15 months of age. Of these households, 2331 were re-interviewed at endline (implemented between June and August 2017). LEAP 1000 payments commenced in September 2015. This panel design is justified over a cross-sectional design, as no new beneficiaries were added after baseline. At endline, we found high level of compliance in the treatment group (88.3%). Thus, we focus on intention-to-treat (ITT) estimates. For robustness, we also examine average treatment on the treated (ATT), and results were very similar.

The qualitative component of the evaluation included in-depth interviews of a cohort of 20 beneficiary women from the treatment arm at baseline, 12 and 24 months’ follow-up. Male partners of beneficiaries were interviewed during the 12-month and 24-month follow-up visits. The purposive sample of the embedded cohort focused on geographical location (remote vs closer to markets) and parity (first time mother vs women with 3+ children) to facilitate comparative analysis.

Study registration

The trial is registered in the International Initiative for Impact Evaluation’s (3ie) Registry for International Development Impact Evaluations (RIDIE-STUDY-ID-55942496d53af).

Patient and public involvement statement

Patients were not involved in this study. The development of the initiative being evaluated, research questions and outcome measures were informed by a vulnerability analysis which indicated that marginalised populations eligible for premium fee waivers under the NHIS were often not enrolling in the scheme. Research findings from the larger impact evaluation were disseminated in March 2018 to national policymakers and stakeholders, including district welfare officers, who liaise directly with programme participants.

Measures

Primary outcomes included current and ever enrolment in NHIS. For household member aged 5 years and above, a series of questions were asked to the main survey respondent, including whether the individual was covered under any health insurance scheme (NHIS was a response option). Then respondents were asked if the individual had ever been enrolled in NHIS (endline only) and whether the individual currently had a valid NHIS card. Analysing ever enrolment allowed us to further disaggregate those that were not enrolled at endline into those never enrolled and those previously enrolled but not currently holding a valid NHIS card at endline.

For those not enrolled, we examined reasons why, including premium was too expensive, respondent did not realise the card expired, travel time or related cost was too high, lack of awareness that card must be renewed annually, respondent had not been sick, waiting times at renewal location are too long, perceived poor quality of NHIS/preferred services not covered, NHIS office was closed and other reasons.

Qualitative interviews elicited narratives of programme impact within each household and context to facilitate interpretation, probing specifically on enrolment and renewal in NHIS. We used a semistructured guide, audio-recorded and transcribed verbatim and translated all interviews. All interviewers and participants were matched on gender and local language preference.

Statistical analyses

Our analytical sample included individuals who were interviewed both at baseline and endline. We performed stratified analyses by age: children aged 5 to 15 years at baseline and older children and adults aged 16 years and above at baseline and thus aged 18 years and above by endline in order to understand whether impacts vary between children and adults, as households may prioritise enrolment of children. Further, while the programme targeting and sampling criteria were based on pregnant women or women with a child under the age of 15 months, study data were collected on NHIS enrolment of all household members, and therefore we conduct our analysis at both the household and individual level, where the latter includes all household members, not just those targeted by the programme. This is justified because the NHIS fee waiver applies to all LEAP household members, not just the targeted individuals.

We examined balance among background characteristics and outcomes at baseline between treatment and comparison individuals. Then we investigated if attritors differed in background characteristics by treatment status (differential attrition), which could threaten internal validity and unbiasedness of our estimates.

Next, we conducted bivariate analyses to examine background characteristics associated with enrolment status, controlling for PMT score. Categories of enrolment in NHIS included (1) currently enrolled, (2) currently not enrolled but previously enrolled (ever) and (3) never enrolled.

To estimate treatment impacts of LEAP 1000 on NHIS enrolment, we used a difference-in-differences (DID) approach as specified in equation 1:

(1)

(1)

where Y

ijt is a binary variable indicating whether individual i residing in community j is enrolled in NHIS in year t.  is a dummy indicator for individual’s i participation into LEAP 1000, equal to 1 if his or her household is assigned to treatment and 0 otherwise. T

t is a time binary variable, set to 1 if the observation is from the endline survey, and to 0 if it is from the baseline.

is a dummy indicator for individual’s i participation into LEAP 1000, equal to 1 if his or her household is assigned to treatment and 0 otherwise. T

t is a time binary variable, set to 1 if the observation is from the endline survey, and to 0 if it is from the baseline.  is the interaction term between the programme and time dummies. X

ijt includes a set of observed individual (gender, age and age squared in years) and household characteristics (age, gender and education (no formal education vs some education) of the household head; household size and PMT score). The model also controls for community fixed effects, λj, to absorb unobserved-time invariant characteristics of communities. β3 is the intent-to-treat (ITT) impact estimate. Standard errors were clustered at the community level. A key assumption in the DID estimation model is that treatment and comparison groups experience parallel trends over time. However, while this assumption cannot be tested in the current study due to a lack of availability of prebaseline data, we expect the assumption to hold given the high level of similarity between treatment and comparison households (sampled from the same communities) at baseline.

is the interaction term between the programme and time dummies. X

ijt includes a set of observed individual (gender, age and age squared in years) and household characteristics (age, gender and education (no formal education vs some education) of the household head; household size and PMT score). The model also controls for community fixed effects, λj, to absorb unobserved-time invariant characteristics of communities. β3 is the intent-to-treat (ITT) impact estimate. Standard errors were clustered at the community level. A key assumption in the DID estimation model is that treatment and comparison groups experience parallel trends over time. However, while this assumption cannot be tested in the current study due to a lack of availability of prebaseline data, we expect the assumption to hold given the high level of similarity between treatment and comparison households (sampled from the same communities) at baseline.

For the qualitative analysis, we first developed a longitudinal summary for each household, integrating women’s and men’s interviews when both were available, to capture the story of impact over time. We summarised patterns in enrolment and renewals across household members and coded for topics related to NHIS using Atlas.ti software.

Results

At baseline, data for 4736 children and 6865 adults were reported, while at endline, 4197 and 6130 of these children and adults, respectively, remained part of the sample households (11% overall attrition for both age groups; online supplementary appendix figure A1 and table A1). Attrition rates were similar between study arms, and attrition by background characteristics and outcomes did not vary between groups (online supplementary appendix table A2).

Supplemental material

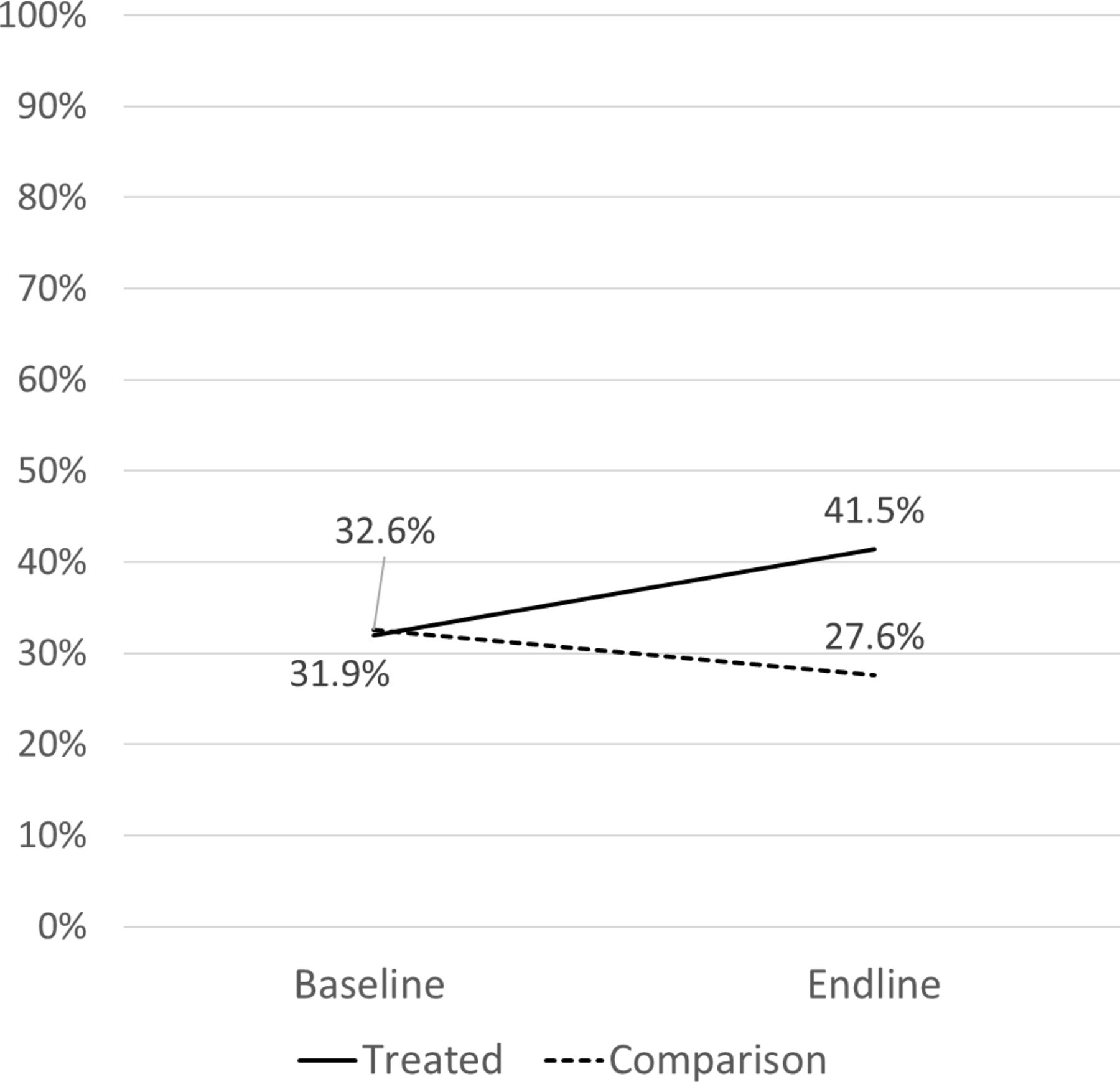

The child sample was 46.6% female, and average age was 8.9 years (SD=2.9), while the adult sample was 56.3% female, and average age was 36.7 years (SD=15.2). Average household size was 7.6 members (SD=3.0), and 6% of households had female heads. Further, 81.9% of heads had no formal education (figures comprise averages calculated from values in Columns 2 and 5, online supplementary appendix table A2). Over the study period, NHIS enrolment increased among the treatment group from 37.4% to 46.6% and decreased among the comparison group from 37.3% to 33.3% (pooled for adults and children; stratified percentages reported in figures 1 and 2).

Proportion of children (5–17 years old) with valid National Health Insurance Scheme card for the current year.

{kind=link}

{kind=link}

Proportion of adults (18+ years old) with valid National Health Insurance Scheme card for the current year.

In bivariate analyses (table 1), characteristics positively associated with enrolment included younger age (current and ever), female (current and ever), higher head education levels (current and ever), female headship (current and ever), smaller households (current and ever) and Karaga district (ever). There were no differences in enrolment by extreme poverty status.

Bivariate analyses of background characteristics by enrolment status, ages 7–103 at endline

Among those previously enrolled but not currently enrolled at endline, the most commonly reported reasons were enrolment fee/premium was too expensive (75.32%; table 2), not realising card expired (11.36%) and travel time/travel cost was too high (9.28%). Qualitative interviews identified barriers to renewal including long wait times, competing demands with work, cost of transport and poor road conditions. Cost was also a salient barrier, reflecting both extreme poverty and confusion about their NHIS fee exemption status. As a male participant in Bongo stated simply, “That money (the transfer) is not even enough to register for the children and the woman.”

Reasons for not renewing/never having NHIS by treatment status, ages 7–103 at endline

Reasons for never enrolment were similar: 65.44% reported enrolment fee/premium too expensive, 14.94% report travel time/travel cost too high, and another commonly reported reason was waiting times (table 2). Some participants described that the LEAP programme had come to their house to take their cards for renewal, eliminating some of the aforementioned barriers. Others described using their LEAP cash transfer to pay for renewal and viewed LEAP as facilitating their enrolment or renewal due to the cash provided by the programme.

Qualitative findings echoed the patterns from the quantitative analyses, with both women and men indicating that women and children were the priority for enrolment. While perceptions of NHIS benefits were generally positive, at baseline several discussed never having enrolled because they questioned the quality of the coverage in terms of types of services included and a perception that medication was not covered (despite the fact that NHIS does cover medications, in and outside of facilities at accredited chemists/pharmacies). There were additional concerns about the quality of care for people using NHIS versus those paying for services, as reflected by a mother in Karaga at baseline.

Some people say when you visit the hospital with it the doctors don’t want to attend to you but if you do not have one, that one they will attend to you. This is the reason why we aren’t interested in it.

Notably, she was enrolled by the endline interview, reflecting the potential impact of the integrated programming on improving acceptance and reducing enrolment barriers.

Impact estimates indicate that LEAP 1000 increased current NHIS enrolment by 14 (95% CI 7.83 to 20.52) and 15 (95% CI 10.63 to 18.46) percentage points for children and adults, respectively (table 3, first two columns). Further, LEAP 1000 increased the proportion of adults reporting having ever been enrolled by 7 (95% CI 0.97 to 12.80) percentage points (table 3, last two columns). The impact on ever enrolment was not significant for children.

Impact estimates of Ghana LEAP 1000 on current NHIS enrolment and ever enrolment, by age groups

Most participants reflected a positive experience or perceptions of NHIS as a way to save costs on healthcare. Among those who had used NHIS, nearly all were satisfied and felt that having insurance had helped them to save money when seeking healthcare. A mother in Karaga identified NHIS enrolment as a major component of LEAP impact, which she further linked to overall poverty reduction.

Now the LEAP 1000 has given us the chance to register for the NHIS and reduced the poverty levels of mothers. It was a big problem for most mothers to get money and register for the NHIS but now it is easy for all beneficiaries of the LEAP programme.

This sentiment was echoed by other mothers who appreciated that being in LEAP had allowed them to enrol and/or renew their families in NHIS and take better care of their family’s health. Some participants discussed lack of medication and other supplies as a barrier to getting care even when you have insurance, as reflected by a father in Bongo, “You know the insurance, when we sent the child, they gave us a prescription to buy medicine because there was no medicine in the hospital.”

Some participants mentioned that in cases like this, they could use their LEAP money to purchase medication, which helped to protect their children’s health.

Discussion

This study demonstrated that an integrated government social protection programme pairing cash transfers with fee waivers for national health insurance enrolment increased enrolment into NHIS among both children and adults. Our findings contribute to the literature on ‘cash plus’ programme by providing evidence of the impact of integrating cash with a health insurance fee waiver to increase enrolment. Virtually all studies to date on this topic have looked at impacts of cash only or conditional cash transfers on morbidity and use of health facilities and have found limited impact, particularly on adult morbidity.2 Our findings highlight a potential pathway through which unconditional cash transfers may improve health, namely, by increasing insurance coverage, which could ultimately lead to increased access to preventive and curative healthcare services.

While impacts on enrolment were significant, enrolment gaps remain, particularly for adults. The salience of cost as a perceived barrier to enrolment both confirms existing research on the topic,13 17 and possible reasons for this finding may include insufficient communication or misunderstanding of the integration of the fee waiver with LEAP. This finding may suggest the need to improve communication with programme participants and/or implementers to maximise the potential impact of this integration and protect against beneficiaries using their transfer to purchase insurance. Additionally, even with the fee waiver, the annual renewal requirement for NHIS can be difficult for poor families to comply with, often leading to expiration of benefits, as highlighted in previous research.15 Such gaps demonstrate operational issues within both programmes that could be better streamlined to ensure that eligible households fully benefit from both services. Extending the validity period for NHIS beyond 1 year for LEAP households, thereby reducing the financial and time burden for annual renewal, is one recommendation. Also, while beyond the scope of the current findings, linking of data systems may be helpful, allowing field officers to track enrolment and validity along with their routine monitoring. Finally, better orientation could be provided to the NHIA workers, ensuring that they do not mistakenly charge fees to exempt LEAP households.

One limitation of this study is that impact estimates are likely lower bounds of programme impacts, given the local average treatment impacts estimated among a sampled treatment group, which is relatively ‘better off” than other LEAP households further from the eligibility cut-off. Another limitation is that at baseline respondents were asked if they are enrolled in any insurance scheme, with NHIS as an option, while at endline, they were specifically about NHIS enrolment in a separate question. However, we do not believe this biases our impact estimates for two reasons. First, given the design, treatment and comparison groups are very similar, therefore we expect the bias in the two groups to be very similar at each point in time. Therefore, in a DID approach these biases cancel out. Second, we believe this bias to be small since in practice NHIS is the only insurance available in these communities. At baseline, less than 0.2% reported having a different insurance. A third limitation is that we did not examine how distance to and quality of health services might moderate programme impacts on enrolment. Finally, qualitative interviews did not cover implementers, which could have provided important insights on communication related to fee waivers, reasons for perceived costs barriers and implementers’ own understanding of the fee waiver process.

Findings underscore the need to improve education among beneficiaries around the annual renewal requirement and exemption from paying premiums. Our data do not allow further investigation as to why respondents—who should be eligible for fee waivers—reported costs as a major barrier to enrolment, and future research should examine this further. Such findings have implications for Ghana and other countries looking to integrate their cash transfer programme with access to health services, which must be done not only at policy level but also with practical implementation modalities for the end user.

Moreover, access to health insurance can help reduce barriers, but alone does not ensure access to healthcare. Individuals can enrol but still face barriers to access related to distances to facilities, quality of services offered and attitudes of staff, among others. This study has demonstrated how integrated programming can improve enrolment rates, but large gaps remain. Future research should investigate how to promote continued enrolment, as well as how integrated cash plus programme can achieve impact on health outcomes beyond access to care, including morbidity, mortality and mental health.

Acknowledgments

The authors would like to acknowledge the support of the Government of Ghana’s Ministry of Gender Children & Social Protection (MoGCSP) and the LEAP Management Secretariat (LMS) (in particular William Niyuni from LMS and Mawutor Ablo from MoGCSP) in the implementation of this evaluation. In addition, the UNICEF Ghana team was instrumental to the success of this evaluation: Sara Abdoulayi, Luigi Peter Ragno, Jennifer Yablonski, Sarah Hague, Maxwell Yiryele Kuunyem, Tayllor Spadafora, Christiana Gbedemah and Jonathan Nasonaa Zakaria. Funding for this evaluation has generously been provided by the United States Agency for International Development. We would also like to acknowledge the hardworking field teams of Institute of Statistical, Social and Economic Research (ISSER) and Navrongo Health Research Centre (NHRC), who conducted the data collection for this study to the highest standards. ISSER: Bashiru Yachori (supervisor), Timothy Magan, Kotin Takibeni Rita, Nasira Iddrisu, Rose Sandow, Amidu Shamsudini (supervisor), Ayisha Musah, Eunice Nfai, Sadia Abdulai, Abdul-Kaharu Tuferu (supervisor), Abukari Sana, Amadu Florence Teni, Faustina Larten, Sampson Kwakwa (supervisor), Ammal Abukari, Akantae Florence Abito, Priscilla Woa, Ayaaba Nancy Assibi, Boakye Acheampong (supervisor), Monica Yeri, Agana Patience, Doreen Akolgo, Jennifer Mengba Dokbila, Alhassan Saibu (supervisor), Mahamoud Mohammed Yusif, Sumaya Iddrisu, Wuni Abigail and Ayishetu Adam. NHRC: Fali Mustapha, Abu Alhassan Safianu, Kusumi Ibrahim, Moro Ali, Peace Akanlerige and Bintu Kwara. Most of all, our highest appreciation goes to the Ghanaian households who were kind enough to give us their time and tell us their stories.

Footnotes

Twitter @tiapalermo

Collaborators UNICEF Office of Research – Innocenti: Tia Palermo (co-principal investigator), Elsa Valli, Richard de Groot; Institute of Statistical, Social and Economic Research, University of Ghana: Isaac Osei-Akoto (co-principal investigator), Clement Adamba, Joseph K. Darko, Robert Darko Osei, Francis Dompae and Nana Yaw; Carolina Population Center, University of North Carolina at Chapel Hill: Clare Barrington (co-principal investigator), Gustavo Angeles, Sudhanshu Handa (co-principal investigator), Frank Otchere, Marlous de Miliano; Navrongo Health Research Centre: Akalpa J. Akaligaung (co-principal investigator) and Raymond Aborigo.

Contributors TMP, EV, GA-T, MdM, CA, TRS and CB were involved in the study design, interpretation of data and contributed to drafting of the article. TMP, EV, GA-T, MdM, CA, TRS and CB had access to the data. TMP and EV wrote the first draft of the manuscript and all authors critically reviewed the manuscript and contributed to writing the final draft. EV carried out statistical analysis, and EV, GA-T, CA and TMP contributed to modelling and interpretation of statistical analyses. MdM and CB conducted qualitative analysis. TMP, EV, GA-T, MdM, CA, TRS and CB approved the final version. A majority of the work for this paper was completed while the corresponding author (TMP) was affiliated with UNICEF Office of Research – Innocenti and she has since moved to the University at Buffalo (SUNY).

Funding Funding for this study was provided to the United Nations Children’s Fund by the United States Agency for International Development and the Canadian International Development Agency. The funders did not play any role in the data collection, analysis or interpretation of findings.

Competing interests None declared.

Patient consent for publication Not required.

Ethics approval The quantitative component was reviewed by the Ethics Committee for the Humanities of the University of Ghana and the qualitative component by the Institutional Review Boards at University of North Carolina at Chapel Hill and Navrongo Health Research Centre.

Provenance and peer review Not commissioned; externally peer reviewed.

Data availability statement No data are available.